Buying into Cogent Communications' Hidden Value

Not my regular quality investment, but the value is just too high versus the price I pay.

Welcome to Compound & Fire, where I’m building wealth the smart way by investing in top-quality businesses that drive long-term shareholder value, paving the path to financial freedom. Join our Global Quality Investing Discord and Substack community to grow this journey together!

Hidden Value: Building a Stake in Cogent Communications

As a self-proclaimed quality investor, someone who gravitates toward predictable cash cows with fortress balance sheets and pristine growth trajectories, Cogent Communications Holdings (NASDAQ: CCOI) initially struck me as the antithesis of everything I hold dear. But a US friend insisted me to look at it. Also my Discord quality investing friends and my Substack audience voted clearly Yes to look into this company. And with a reason!

At first glance, it's a textbook value trap: saddled with towering debt levels exceeding $2.3 billion, posting net losses amid a transitional phase, and topped off with the optics of its founder-CEO offloading the shares of his holdings. For purists like me, these are glaring red flags, signals of distress in a sector notorious for value destruction.

Yet, after peeling back the layers, I have bought a stake at $37.80 today. What emerges isn't a flawed relic of the telecom bust, but a coiled spring of underappreciated assets and catalysts poised to propel it toward a rerating. This is a classic deep-value setup, where the market fixates on near-term warts while overlooking the transformative potential beneath. Compounding the appeal is a powerful tax shield: Under the impacts of the H.R. 1 tax bill, Cogent anticipates zero federal income tax liability for at least the next five years (through 2030). This isn't a temporary quirk, it's rooted in carried-forward net operating losses from the Sprint integration and legacy operations, preserving every dollar of EBITDA for reinvestment, debt paydown, dividends, or buybacks. In a high-interest environment, this cash retention acts as a stealthy multiplier for shareholder returns, effectively boosting free cash flow yields by 25–30% versus taxable peers.

The Sprint Deal: A $1 Bargain with a $700 Million Kicker

The pivot point for Cogent's story traces back to its audacious 2024 acquisition of Sprint's wireline assets from T-Mobile, a move that, on paper, looks like financial wizardry dressed in legacy telecom drag. The rationale was straightforward: scoop up a dormant, underutilized infrastructure empire at rock-bottom cost to fuel Cogent's pivot into high-margin optical transport and data center plays, while offloading the baggage of a shrinking enterprise unit.

What did Cogent actually buy? For a nominal $1, it inherited Sprint's crown jewels: 19,000 route miles of intercity fiber (laid along railroad rights-of-way between 1985 and 1992 at a $20.5 billion historical capex), 1,200 miles of metro fiber, and 482 central office buildings totaling 1.9 million square feet with 230 MW of inbound power. This wasn't just pipes and bricks; it was a ready-made backbone for modern bandwidth-hungry applications, mothballed since 2015 after Sprint's voice-era heyday. Bundled in was Sprint's Global Mobile Group (GMG) enterprise business, serving multinational giants with dedicated internet access and MPLS VPNs, but that came with a twist: T-Mobile effectively paid Cogent $700 million over 54 months as a subsidy to assume the troubled unit, which had been losing ground at a 10.6% annual rate prior to the acquisition.

As of Q2 2025, the net present value (NPV) of the remaining T-Mobile subsidy stands at $244 million, with monthly payments locked in through October 2028. This figure comes straight from Cogent's disclosures: It's the discounted value (at Cogent's ~8% cost of capital) of the outstanding ~$333 million in gross payments (averaging ~$8.3 million/month, or ~$25 million/quarter equivalent) over the next 40 months. These aren't fluffy projections, they're ironclad contractual obligations, providing predictable, non-dilutive cash that management treats as a balance sheet receivable for leverage calculations. By 2028, the tail end could contribute another ~$100 million in annual inflows (prorated for the partial year), acting as a reliable buffer during the wavelength ramp.

The Debt Dilemma: Integration Costs, Not Reckless Overreach

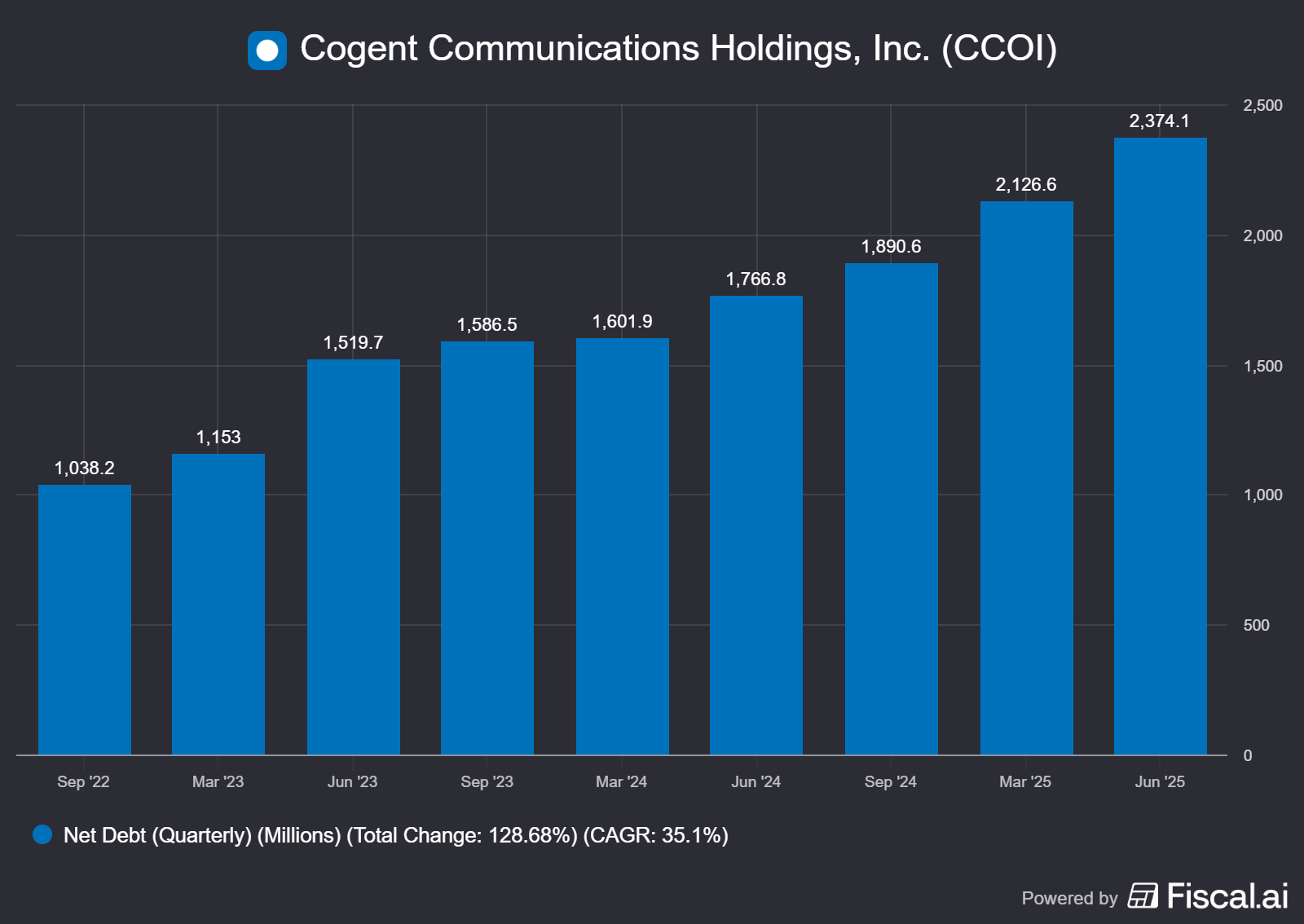

If the Sprint assets were a steal, why the debt explosion? Total borrowings ballooned to $2.34 billion by mid-2025, pushing net leverage to a eye-watering ~10x trailing EBITDA.

Critics point fingers at overleveraged folly, but dig deeper: this isn't profligate spending, it's the price of unlocking value from a fire-sale acquisition.

Post-close, Cogent poured capital into reactivation. Over 18 months, it reconfigured the fiber for wavelength delivery (point-to-point optics at 10/100/400 Gbps) and gutted the buildings—ripping out 23,500 bays of obsolete phone switches configured for -48V DC power—to convert them into data centers. This added 125 facilities to its footprint, swelling total square footage to 2 million and AC power capacity to 212 MW (from a pre-deal 55 sites). Capex spiked accordingly: LTM spend hit $219.6 million through Q2 2025, largely on these buildouts and network grooming. CEO Dave Schaeffer has guided that outlays peaked at ~$225 million in 2024 (driven by Sprint integration) but will taper to $150 million annually as the heavy lifting wraps, freeing up ~$75 million in yearly cash flow for deleveraging or returns.

Recent refinancings underscore discipline: A $600 million 6.5% secured note issuance in June 2025 extended maturities out to 2032 (from 2026) and added $100 million in liquidity, while a $174 million IPv4-backed securitization in April trimmed blended rates to 6.6%. Far from a debt spiral, this is tactical refinancing amid asset monetization, setting the stage for meaningful relief, especially with the tax benefits supercharging cash generation and the T-Mobile payments providing steady deleveraging support.

Buried Treasure: Data Centers and IPv4 as Untapped Goldmines

Here's where the value thesis ignites: Cogent's balance sheet, at historical cost under GAAP, masks a treasure trove. Property, plant, and equipment sits at a modest $1.725 billion net book value as of Q2 2025, essentially the low acquisition basis spread over decades of depreciation. But fair market? A different story.

Start with the data centers: Of the 180 facilities, 24 non-core sites (1 million sq ft, 109 MW) are ready for divestiture, with Cogent already receiving multiple letters of intent (LOIs) for these or similar assets, signaling strong buyer interest. Comps suggest $1.1–$1.9 billion in proceeds at $10–$17 million per MW. At a midpoint $1.5 billion sale (implying a ~6.7x book multiple), this alone shaves ~64% off total debt, dropping it to ~$840 million. Interest expense? Currently ~$150 million annually at blended ~6.5% rates; post-sale, it plummets to ~$55 million, a $95 million annual tailwind to the bottom line.

Layer in IPv4 addresses: Cogent holds 38 million (13.2 million leased), carried at $458 million book but worth $760 million–$1.14 billion at $20–$30 apiece amid ongoing scarcity. The leased block alone yields $60 million annualized revenue (up 40% YoY), and further securitizations (like the recent $174 million tranche) could unlock $300–$700 million more without outright sales. These aren't speculative; they're liquid digital real estate, with average lease pricing up 22% YoY to $0.39 per address.

Combined, partial monetization could inject $1.8–$2.6 billion in liquidity, enough to erase net debt entirely and ignite a balance sheet renaissance.

The Growth Inflection: Wavelengths Lead, Legacy Stabilizes

With the Sprint purge nearing completion (unprofitable contracts expiring), revenue troughs behind: Q2 2025 service revenue dipped 0.3% QoQ to $246 million, but sequential declines halved to $0.8 million, signaling mid-Q3 positivity. On-net revenue (high-margin, direct-connect) grew 2.1% QoQ to $132 million, while off-net revenue (partner-dependent) fell 4.8% to $102 million—trending toward stabilization at low-single-digit declines. Non-core legacy (acquired voice relics) shrinks ~$2.7 million quarterly, a drag that's fading.

The accelerator? Wavelength services, a startup within Cogent exploding from $3.6 million in Q2 2024 to $9.1 million last quarter (150% YoY). Targeting a $2 billion TAM, management eyes 25% share by 2028 (~$500 million run-rate) via four unbeatable edges:

Endpoint reach into 938 sites

90% unique routes for diversity

Aggressive pricing off the $1 Sprint acquisition basis (20% discount to competition)

Superior fiber reliability

The 30 day provisioning speed mentioned by Schaeffer as a USP is fast, but not a clear differentiator. Competitors Lumen's 20 days and Zayo's 24 hours (on-demand) show the competition is catching up or leading in speed for select routes. Cogent's edge may lie more in its unique routes and pricing rather than pure velocity.

AI data center interconnects are the turbocharger, with a 4,687-unit funnel and connections up 95% YoY. Overall revenue? 6–8% long-term CAGR to ~$1.5 billion by 2028.

Margins follow: Adjusted EBITDA hit 29.8% in Q2 (up 200 bps QoQ to $73.5 million), with guidance for another ~200 bps annual expansion, potentially for a decade (!), as on-net product mix rises and wavelengths (near-90% gross margins) scale. The tax shield amplifies this: Zero federal taxes mean full EBITDA flow-through to cash, turbocharging FCF without Uncle Sam's cut.

The CEO Sell-Off: Distress, Not Desertion

No discussion is complete without addressing Schaeffer's share dumps, over 2.66 million liquidated in August 2025 alone, slashing his stake from 9% to 1.4% year-to-date.

At surface level, it's alarming: a founder cashing out amid volatility screams misalignment. Reality? A brutal margin call cascade. JPMorgan and RBC seized $82 million in pledged shares after Cogent's stock plunged post-earnings, triggered by Schaeffer's broader woes: a $1.1 billion D.C.-area commercial real estate portfolio (42 buildings) that's shed $600 million in value since 2022 amid COVID vacancies (now 35%) and sluggish sales. Loans backed by Cogent stock backfired as shares dipped below thresholds; sales were "under duress, most... completely involuntary," per Schaeffer, who draws no salary and relies on dividends/stock awards. He's negotiating lender extensions, but this personal storm, completely unrelated to Cogent ops, clouded perception without tainting fundamentals. Audit reviews found no material company risk. Schaeffer was diversifying his money and betting on two horses: Cogent and the commercial real estate business. As you can see, diversifying isn’t always good. His commercial real estate business is now hurting his Cogent ownership significantly. Must be very difficult for a founder to see this happening.

A 2028 Snapshot: From Losses to $400 Million+ Free Cash Flow

To quantify the arc, consider this adjusted 2028 bridge (conservative, excluding full asset sales). It starts with management's multiyear targets: $1.5 billion revenue (6% CAGR from $984 million run-rate), driven by $500 million wavelengths (+140% CAGR), 5% core on-net/off-net growth, and non-core normalization. EBITDA hits $500 million (33% margin, +400 bps from today via 200 bps annual gains).

Subtract interest at $55 million (post-$1.5 billion divestiture deleveraging to $840 million debt at 6.5%), capex at $150 million, and taxes at negligible. Add the ~$100 million T-Mobile residual (full-year equivalent from the $244 million Q2 NPV tail, prorated for 2028's partial overlap with the 40-month stream at ~$8.3 million/month). Operating cash flow approximates $445 million (EBITDA - interest - taxes, plus non-cash addbacks). After capex, FCF lands at ~$278 million.

For net income, layer in estimated D&A of ~$180 million (based on current $182 million quarterly run-rate, adjusted for post-sale asset base and growth capex). This yields NI ≈ ($500M EBITDA - $180M D&A - $55M interest) × (1 - 0% tax) + $100M T-Mobile/other = $300–$350 million range (midpoint $325 million, allowing for WC changes and IPv4 ramps). With ~49 million shares outstanding (current fully diluted basis, net of modest buybacks), that's $6–$7 per share, a swing from today's losses. But the 100M T-Mobile is gone after 2028.

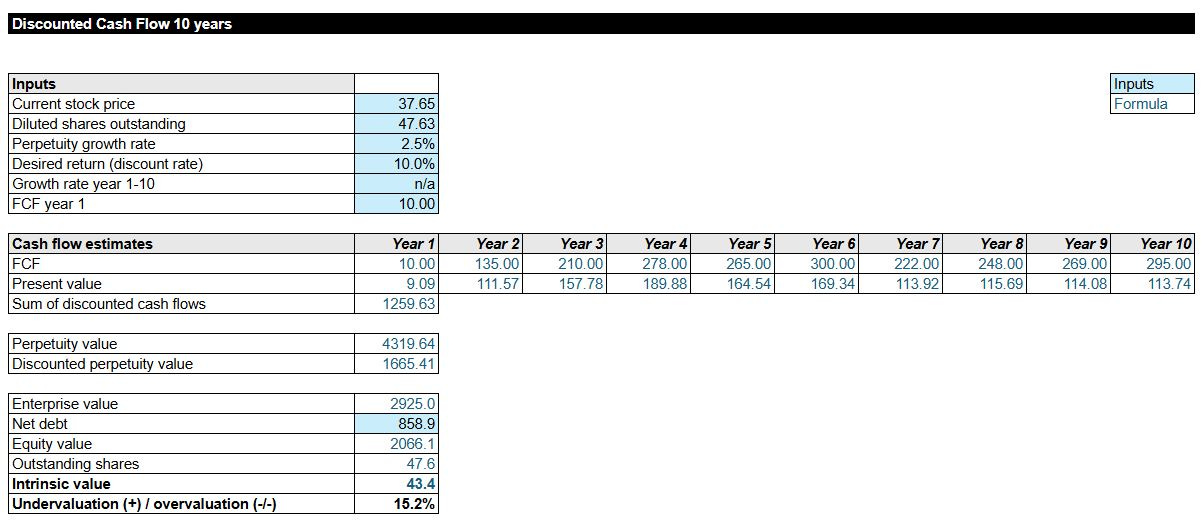

So it’s good to run a DCF model and insert all expected cash flows for the next ten years given the expected revenue growth and increased margin because of improving product mix and especially the wavelength business to kick in. With a 10% desired return and an FCF for year 1 of just 10 the undervaluation is 15.2%. I have considered the divestment of 24 data centers and hence net debt to improve by 1.5B. As Cogent already received LOI’s I expect this to happen within the next months and this could be a catalysator for the stock price. Also after 2030 I considered Cogent will have to pay 21% tax, so that is why FCF is dropping in year 7.

Un undervaluation of 15.2% might doesn’t sound wild, but the real value is in their assets which have way more value than their current market cap and which gives a floor towards the stock price in my opinion.

Is the dividend high? Yes, it is close to 200M a year at the moment, so 2025 and 2026 they are paying more than the cash inflow, but from year 3 onwards it’s covered. Cogent doesn’t need more capex to grow, investments have been made.

So expect a 10% yearly return, paid in dividends, an upside of 15% to get back to intrinsic value and a free call option for the hidden value of their assets.

I think this case looks quite solid, but given the high debt it’s important that the divestment of these data centers will happen and the revenue of the wavelength business to grow towards 500M in 2028. Because of the cost advantage and the high reliability management of Cogent states this 500M as conservative.

Another “risk” is that Cogent is seen as an acquisition target. Just a high-over calculation of the assets minus the debt: ~1.5B for 24 data centers + remaining 156 core data centers ~8.3B plus the IPv4 adresses ~0.9B (38M * $25) = $10.7B minus net debt $2.4B is $8.3B. At a market cap of $1.9B this could easily get the attention of companies like:

Digital Realty Trust, which is the largest global data center operator with 300+ facilities. They're expanding edge/colocation for AI interconnects, and Cogent's urban, fiber-dense sites fit their hybrid strategy.

Equinix, which focuses on interconnected ecosystems (1,000+ DCs). Cogent's edge sites with built-in fiber (19K+ route miles) could enhance their xScale platform for hyperscalers.

Blackstone Inc. (via QTS Realty Trust): PE giant with $108B+ in 2025 data center deals; QTS is their vehicle for hyperscale/edge builds. They'd value Cogent's power-ready sites (212MW) amid scarcity, plus IPv4 for cloud ops. Blackstone acquired AirTrunk for $13B in 2024; $3.8B for Cogent (double today’s price) would be a bargain at ~$18M/MW vs. $30M+ comps.

Other companies like Microsoft, Amazon, KKR (via CyrusOne), Lumen Technologies, Zayo Group or Iron Mountain.

I have to say that Cogent's DCs are small/low-density (not hyperscale-grade), and a deal would include non-DC assets like wavelengths and an enterprise in decline. CEO Schaeffer draws no salary, he relies on dividends, and has no sale signals. His focus is on wavelengths and growing this market, so can imagine he isn’t very interested in an acquisition, but with his ownership reduced his influence in the company reduced.

As a shareholder I am going to track the development of Cogent Communications closely! Although it’s a value play instead of a quality play, I think the odds of winning outweigh the odds of losing with a very interesting risk-reward profile.

Disclaimer

The information in this article is provided for informational and educational purposes only.

The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any mistakes or investment decision made by you. You are responsible for your own investment research and investment decisions.

Thank you for bringing this idea forward. I know the quality investing community does not like making investment based on SOTP or P/NAV, but they they are probably the right approach in valuing this business quickly. With the DCs and IPv4 valued at $10.7B at the current market rates, minus net debt of $2.4B we get a NAV of $8.3B. The additional T-Mobile payment has a NAV of $244M at 8% discount rate. So we have P/NAV = 0.22X. Then we have the high-growth Wavelengths business on top as a free option. It seems to me the R/R is very attractive even if we have a shallow recession or slowdown in AI or internet traffic needs. I think the key risk to the investment case is CEO Dave Schaeffer's ability to unlock the value of the assets. Judging from his track record, I think there is a pretty high probability he can do it. I know the DCF model looks more scientific, but in this case, it might not be very useful. I have followed Arnold into this investment.

Great article, I just got gutted with the sell-off last week, looking for arguments to double down / cut my losses now, that's how I found this article.