Computer Modelling Group: New Compounding Star at the Horizon

In December I have add Computer Modelling Group ($CMG) to my portfolio and in the mean time the company became even more attractive. In this article I will share why I decided to buy CMG.

Welcome to Compound & Fire! We search for businesses which create strong shareholder value over time in order to get financial independence and retire early. Join for free if you haven’t subscribed yet.

General information

Name: Computer Modelling Group

Logo:

ISIN: CA2052491057

Ticker: CMG.TO

Country: Canada

Current market cap: 845M CAD

Share price: 10.27 CAD

Outstanding shares: 81.85 million

Free float: 80.26 million

Average daily volume: 126.57k

About: Computer Modelling Group Ltd. is a tech wizard for the energy industry, creating powerful software that helps companies understand and manage oil and gas reservoirs hidden deep underground. Their tools are like high-tech crystal balls, allowing engineers to predict how these reservoirs will behave over time and make smart decisions about extracting resources. By combining cutting-edge science with practical know-how, CMG helps energy companies work more efficiently and tackle complex challenges in the ever-evolving world of energy production.

Source: IR Presentation CMG

Quick Scan

"Protecting your money is like guarding a castle: it's easier to keep invaders out than to reclaim lost territory.”

That is why I look for moat companies which protect my castle. I want to minimize the risk of losing money and maximize the chance a company is compounding. Compounding is like a snowball rolling downhill, getting bigger and faster as it goes, just as a company's profits grow faster when they reinvest their earnings into high-return projects, making even more money to reinvest again and again.

Balance sheet

A low Net debt / FCF ratio indicates that a company can repay its debt faster using its free cash flow, potentially leading to better long-term shareholder return:

Net debt / FCF: 0, CMG has a net cash position (Net debt / FCF < 4x ✅)

A rule of thumb suggests that companies with a goodwill to assets ratio higher than 30% should be carefully analyzed to ensure the risk of potential write-offs is low:

Goodwill / Total assets: 2.7% (Goodwill / Total assets <30% ✅)

Impairments last 10 years: 0 (Impairments / Goodwill < 10% ✅)

Cash Flow

“A business that doesn't take any capital and grows and has almost infinite Returns on required Equity capital is the ideal business” (Warren Buffett)

That is why I look for asset-light companies.

Capex / Sales: 0.6% (Capex / Sales <5% ✅)

Capex / Operating Cash Flow 2.5% (Capex / Operating Cash Flow <25% ✅)

Operating Cash Flow (OCF) / Net Income 137% (OCF / Net Income >80% ✅)

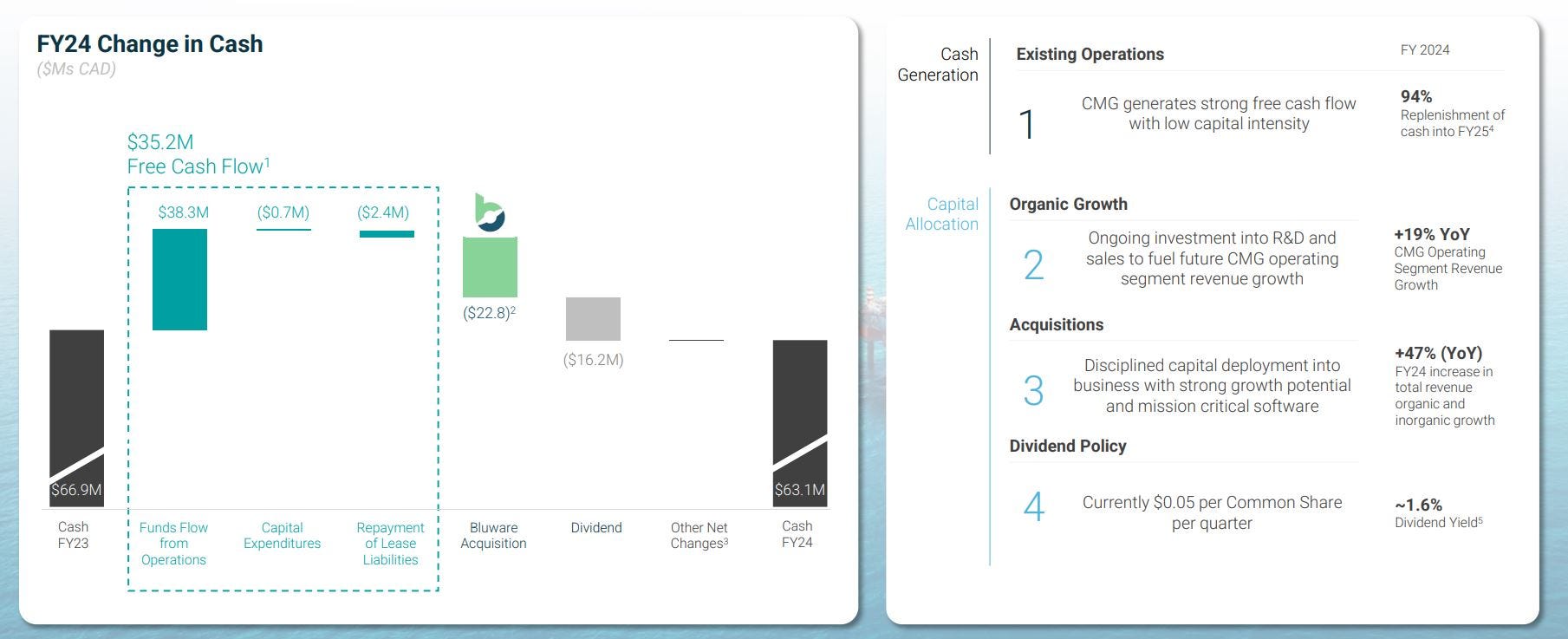

Here is a bridge between FY 2023 and FY 2024 cash, where you can see they have used a big portion of the cash for the Bluware acquisition. If you have an asset-light model you can spend most of your income towards acquisitions. On the right side the new strategy with a strong focus towards capital allocation, which I like to see:

Source: IR Presentation

Capital Allocation

“Capital allocation is the CEO’s most important job” (Warren Buffett)

The metric which most often tells most about capital allocation is ROIC.

Return on Invested Capital: 26.7% (ROIC >15% ✅ )

Profitability

A high gross margin provides significant insights into a company's competitive advantage and potential for long-term shareholder returns.

Gross Margin: 80.3% (Gross Margin >40% ✅)

Net margin: 16.4% (Net Margin > 10% ✅)

The net profit margin is declining, but this is mainly caused by the amortization of goodwill and intangible assets as a result of their acquisitions in 2023 and 2024.

Stock-Based Compensation (SBC)

95% of Restricted Stock Units (RSUs) are sold on vest, which potentially defeats the purpose of giving employees long-term skin in the game (Bill Gurley, a well-known venture capitalist).

Companies offering stock-based compensation plans can benefit shareholders through higher stock prices, but only if the level of dilution is not excessive.

Two different views, but opposite. In general I want to see the stock-based compensation below 5%, else it will dilute my stake in a company.

SBC: 2.6% (SBC < 5% ✅)

SBC has been declining for CMG and beginning as of fiscal year 2024 bonuses to employees will be awarded as a combination of cash and a contribution to a share purchase plan. Cash allocated toward the equity portion of the bonus will be used to purchase CMG shares on the open market on the employee's behalf. This structure allows employees to build a meaningful investment in the company, think like owners, and participate in our future success without the dilution of security-based compensation arrangements.

Change in Shares Outstanding 10 yrs: +3% (Change in Shares Outstanding <10% ✅)

Conclusion Quick-Scan

The quick scan shows a perfect score for Computer Modelling Group! Hence I continue my analysis of the company.

Management

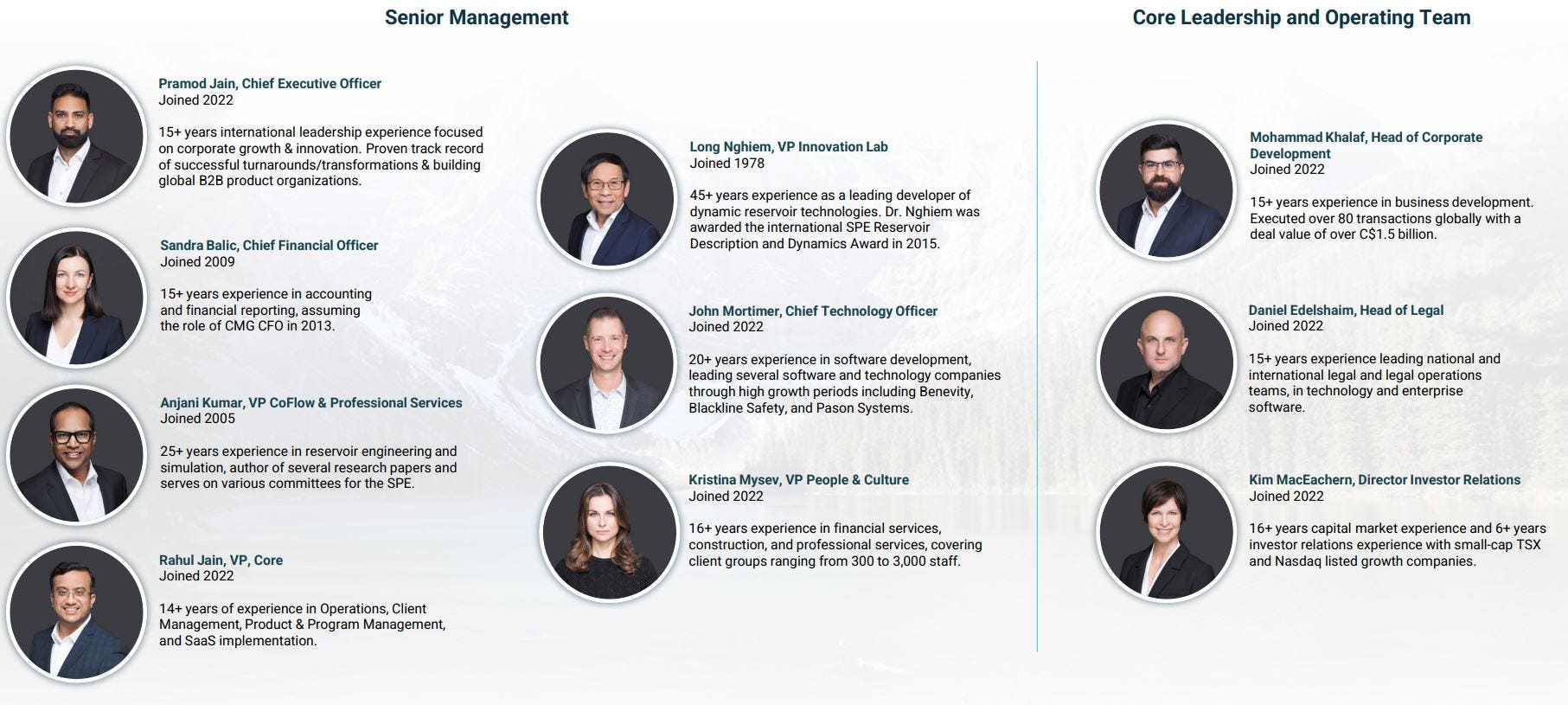

Pramod Jain – CEO (since 2022, 0.12% interest in CMG) Mr. Jain is a software executive and professional engineer with over 15 years of international leadership experience focused on corporate growth and innovation. Mr. Jain is transforming the business: focus on long-term, focus on capital allocation (M&A), align the interest of management with the shareholders, reduce dilution of the number of stocks and add ROIC as a metric internally for the board. Just read the CEO letter to shareholders (first pages of the annual report 2024) and you probably will get as excited as I am. Here you can listen to a great interview from 2023 with Pramod Jain:

John Mortimer – Chief Technology Officer (since 2022, 0.01% interest in CMG). As the Chief Technology Officer for CMG, John Mortimer is responsible for the advancement, innovation, and enhancement of CMG’s core software offering.

Sandra Balic – Chief Financial Officer (joined in 2009, 0.33% interest in CMG). Sandra is a Chartered Professional Accountant with more than 15 years of experience in accounting and financial management and holds a Bachelor of Management, Advanced Accounting degree from the University of Lethbridge.

Mohammad Khalaf – Head of Corporate Development (since 2022). Mohammad’s background in mergers & acquisitions and strategy, more than 7 years experience as VP M&A at one of the six OpCo’s of Constellation Software, will support business growth through effective capital allocation for new initiatives.

Next to these three chief executives CMG has hired Constellation Software knowledge in their Board of Directors:

Mark Miller – Chairman of the Board of Directors (since 2019). Miller is Chief Operating Officer at Constellation Software.

John Billowits – Member of the Board of Directors (since 2021) and also a board member at Constellation software and a private investor.

An overview on their Senior Management and Core Leadership TeamL

Source: IR Presentation

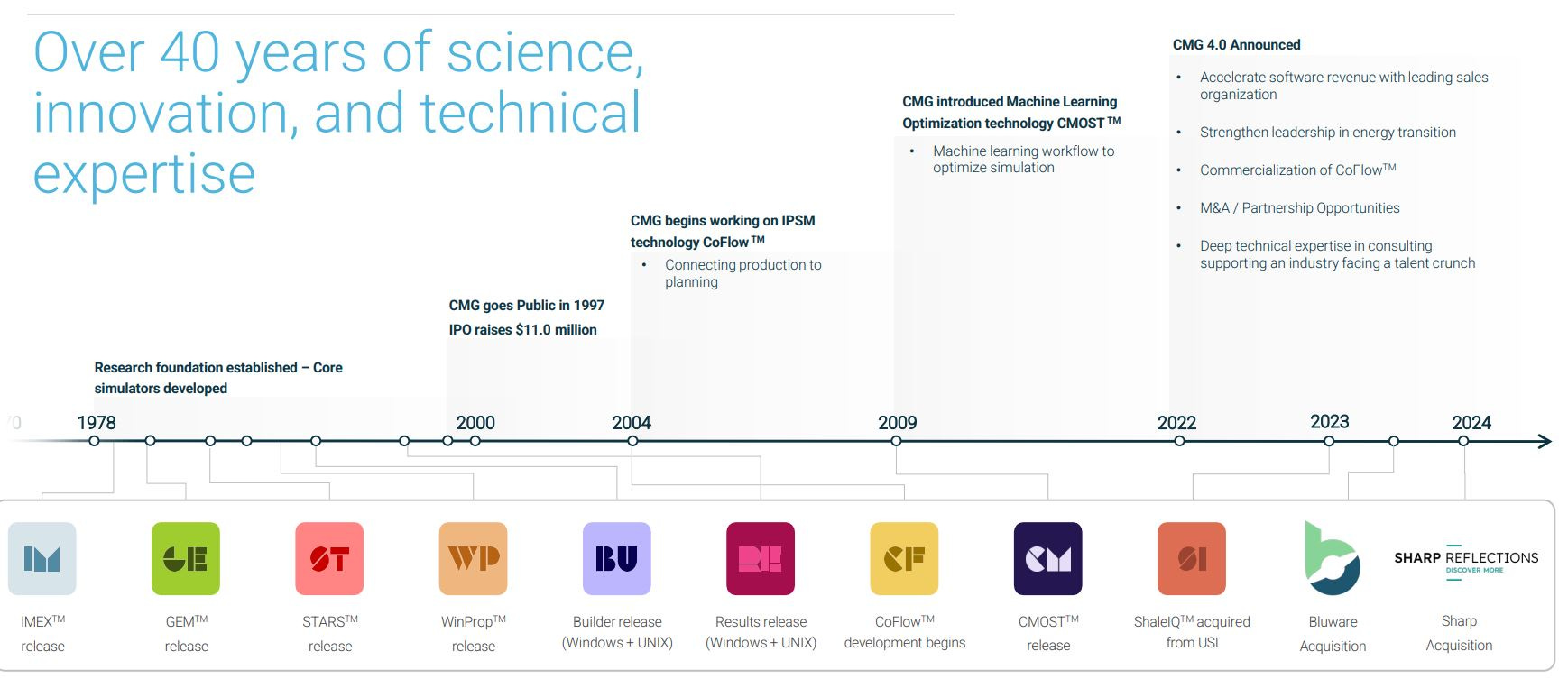

It is clear that as of 2022 Computer Modelling Group started a new strategy and that their structure follows this strategy, hence in 2022 they have announced their new structure.

CMG’s market

Imagine a company that creates super-smart computer programs that help energy companies figure out exactly where and how to dig for oil and gas underground - almost like a high-tech treasure map for energy exploration. Computer Modelling Group (CMG) is that kind of tech company, creating special software that helps energy companies make smarter decisions about finding and extracting valuable resources from deep beneath the Earth's surface. CMG is active in a niche market.

Computer Modelling Group (CMG) has two main business units that serve different parts of the energy market:

CMG Segment: This is like the company's main superpower. They make special computer programs that help oil and gas companies figure out the best ways to get oil and gas from underground. Their software shows what's happening deep beneath the Earth's surface. This helps energy companies make better decisions about where to drill and how to get the most oil and gas out of the ground safely.

BHV Segment: This is CMG's newer superpower. They got this when they bought the company Sharp Reflections in November 2024. BHV makes software that helps energy companies understand pictures of what's under the ground. So it helps companies find where the oil and gas might be in the first place.

CMG is also starting to use its software and services to help with new types of energy, like storing carbon underground or finding places for geothermal energy. This shows they're trying to help with cleaner energy solutions too. Here is where their software is used:

Market characteristics

Niche Expertise: CMG develops complex software that simulates underground reservoirs, which is crucial for oil and gas extraction.

Recurring Revenue: The company benefits from a high contract renewal rate (over 98%), providing stable, predictable income.

Global Reach: CMG serves clients in 58 countries, indicating a broad international market.

Energy Transition: The company is adapting to the changing energy landscape by offering solutions for carbon capture, hydrogen, and geothermal energy.

Computer Modelling Group (CMG) primarily serves the energy industry, with a focus on oil and gas companies. Their main customers include:

International oil companies: CMG has a diverse customer base of international oil companies in approximately 60 countries.

Heavy oil producers: As of 2016, 100% of the top-20 Canadian heavy oil producers were using CMG's software.

Energy transition companies: CMG is expanding its services to companies involved in carbon capture and storage (CCS) projects, as well as other energy transition initiatives.

Exploration and production companies: The BHV segment serves companies involved in seismic interpretation and energy exploration.

Research institutions and universities: CMG provides support and software to educational and research partners in the energy industry.

CMG's software and services are used globally, with the company having sales and technical support services based in Calgary, Houston, London, Dubai, Bogota, and Kuala Lumpur.

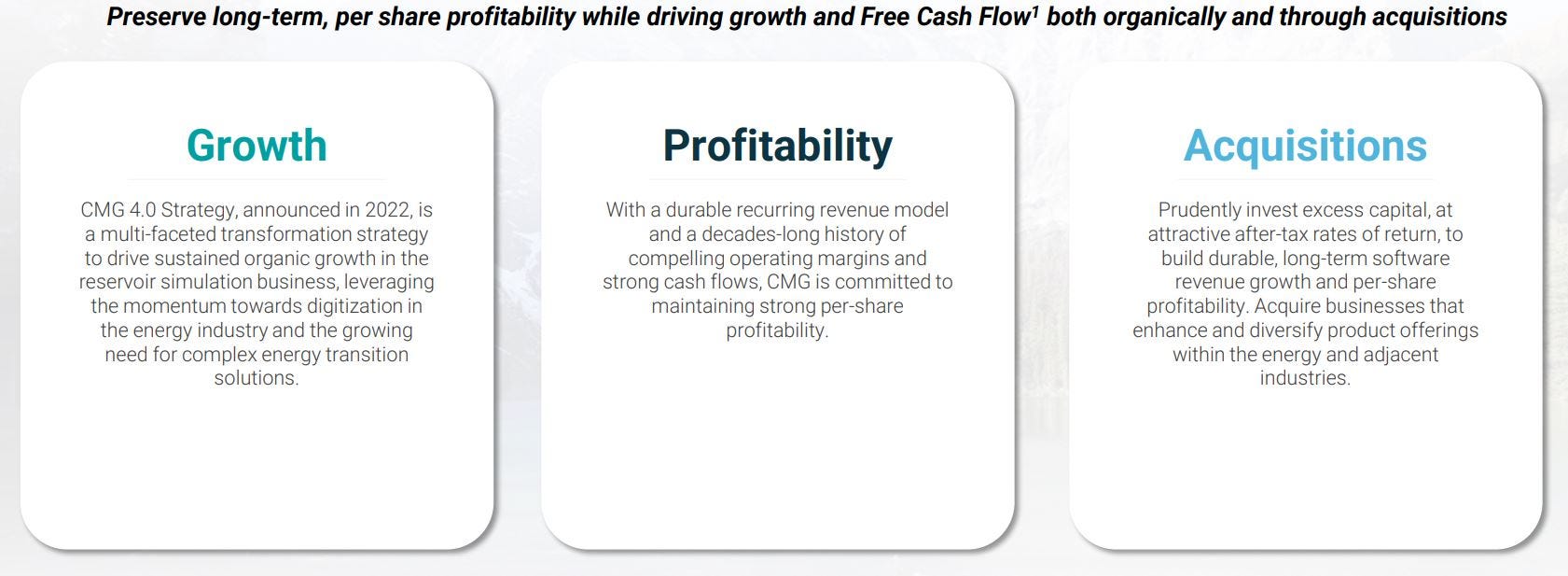

Company’s Strategy

Computer Modelling Group (CMG) has a strategy called CMG 4.0, which they announced in 2022. This strategy is like a roadmap for how the company wants to grow and become more successful. It focuses on three main things:

Source: IR Presentation

One big part of CMG's strategy is moving their software to the cloud. This means customers can use CMG's programs over the internet instead of installing them on their own computers. This cloud strategy helps CMG's customers work more efficiently and access the latest software updates easily.

CMG is also focusing on new energy solutions, like helping companies store carbon underground or find places for geothermal energy. This shows they're adapting to changes in the energy industry.

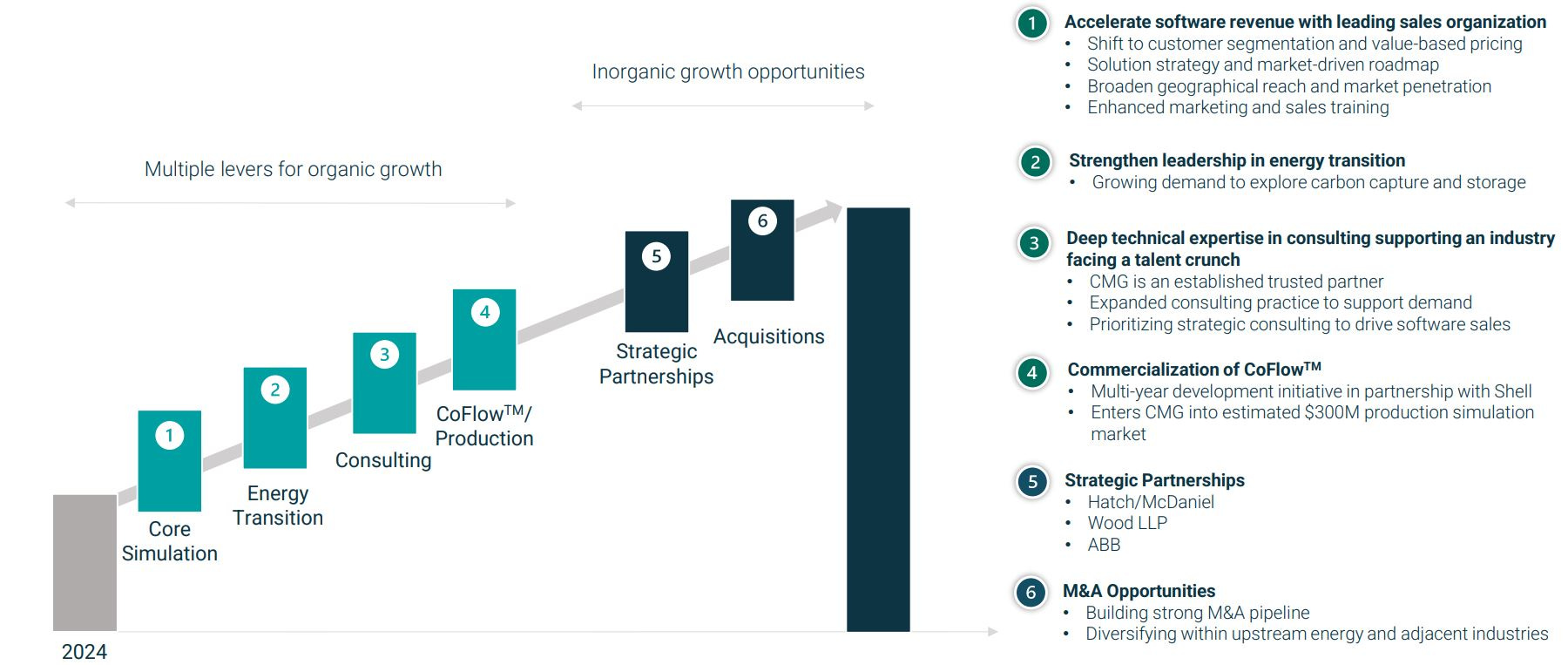

With the new strategy CMG focuses on multiple levers for organic growth and inorganic grouwth opportunities.

Source:IR Presentation

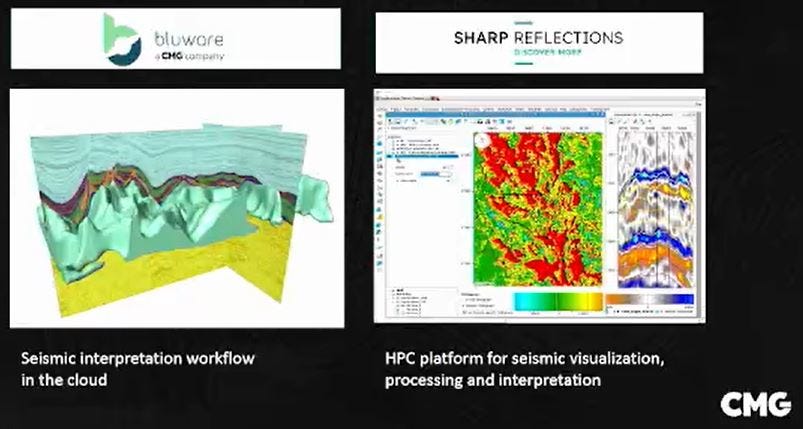

CMG acquired Bluware-Headwave Ventures Inc. in 2023 and Sharp Reflections GmbH in 2024.

Bluware is an open-source software and services company specializing in cloud and interactive deep learning solutions for subsurface decision-making, including seismic interpretation. With huge data interpretation could take up to 8 months. Bluware developed interactive AI, which means the user is still training the machine. It is a labeling tool which gives guidance back to the computer and which saves the user a lot of interpretation time. Here is the logic provided for the Bluware acquisition:

Source: Webcast Bluware

Sharp a cloud-based seismic processing and interpretation platform. Built on modern advancements in high performance computing, it combines prestack seismic data visualization, processing, and interpretation. They serve a global customer base with a lot of supermajors as their customer. Revenue breakdown is 69% software and 31% services and total recurring revenue of 69%. This recurring revenue tells how mission critical CMG is to their customers and how sticky the business is.

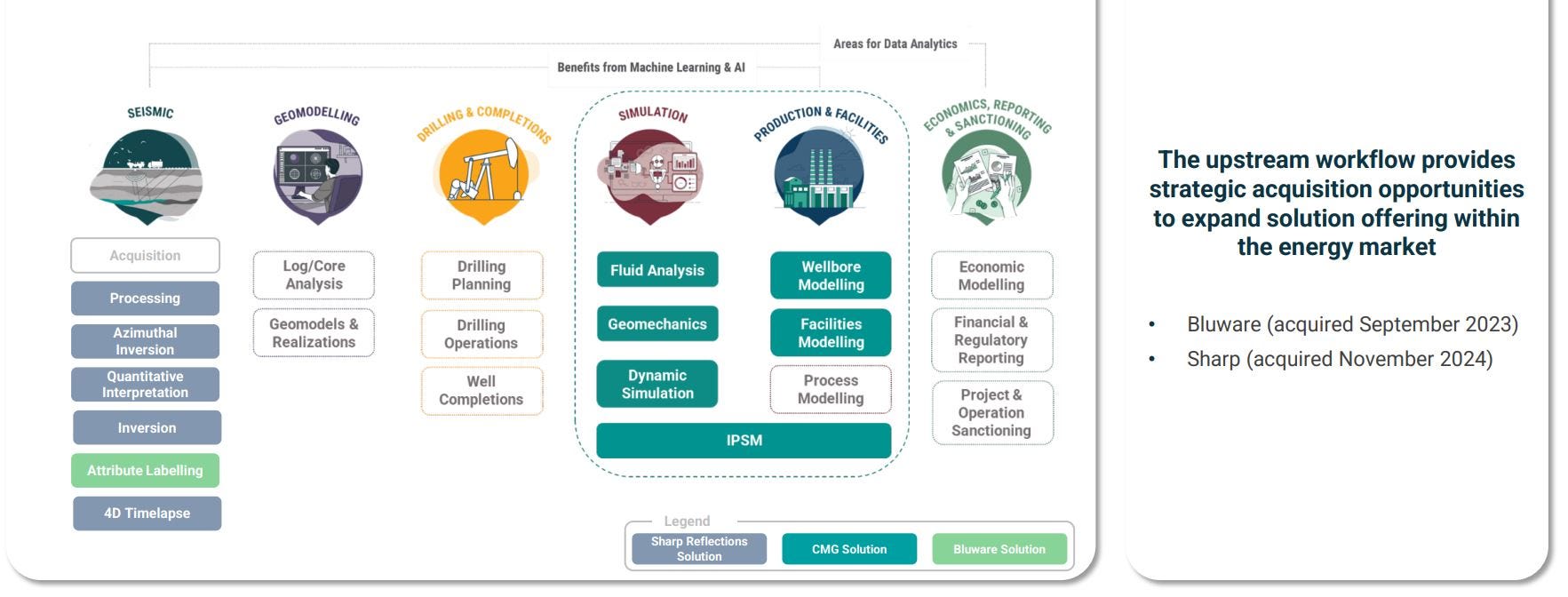

With these two acquisitions you can see in below overview that CMG bought themselves into to Seismic market, while opportunities for acquisitions remain in Geomodelling, Drilling & Completions and Economics, Reporting & Sanctioning:

Source: IR Presentation

Business Model

Computer Modelling Group (CMG) is a software company that makes money by creating and selling special computer programs for the oil and gas industry. Here's how their business model works.

License Sales: CMG sells licenses to use their software. Companies pay to use these programs. There are different types of licenses:

Annuity License Agreements: these include a term-based software license bundled with maintenance. These agreements provide customers with rights to use the software for a fixed term, typically one year, but could be shorter or longer, and include maintenance consisting of customer support and unspecified upgrades.

Perpetual License Agreements: perpetual license agreements grant the customer the right to use the then-current version of software license in perpetuity. This revenue stream is recorded under “Perpetual license” revenue and is recognized at a point in time, upon delivery of the licensed product. Customers purchasing perpetual licenses may also enter into a separate maintenance and support agreement giving them access to customer support and software upgrades. The majority of customers who have acquired perpetual software licenses subsequently purchase a maintenance package.

Because of the revenue recognition and the timing of billings it is best to analyze annual earnings and don’t get distracted by quarterly swings.

Looking at the revenue trend you can clearly see the impact of the new strategy where revenue has grown by a CAGR of 28% since 2022 towards end of 2024.

Customers

CMG has around 650 different customers in 57 countries. 450 of these customers are Oil & Gas customers and around 200 customers are universities. Universities are very important as CMG wants students to get used to their software even before they start working in the Oil & Gas industry. The geographical revenue split for CMG you can see in below map:

Source: Annual Needham Growth Conference

Europe is CMG’s competitive homeground, where CMG wants to get more market share. Europe is less about Oil & Gas but really about energy transition. There is a lot of activity happening in their CCS space, especially in the Northsea. So CCS is a real growth opportunity for CMG. Each different geography has a different geological and hence has a different trend.

Finally, and a very important metric to me: the Net Promotor Score (NPS) which is 68% for CMG, compared to a B2B software average of 41%. This means CMG adds more perceived value to their customers versus their competitors.

Valuation

In order to have an understanding of the valuation of the company it is good to look from multiple angles.

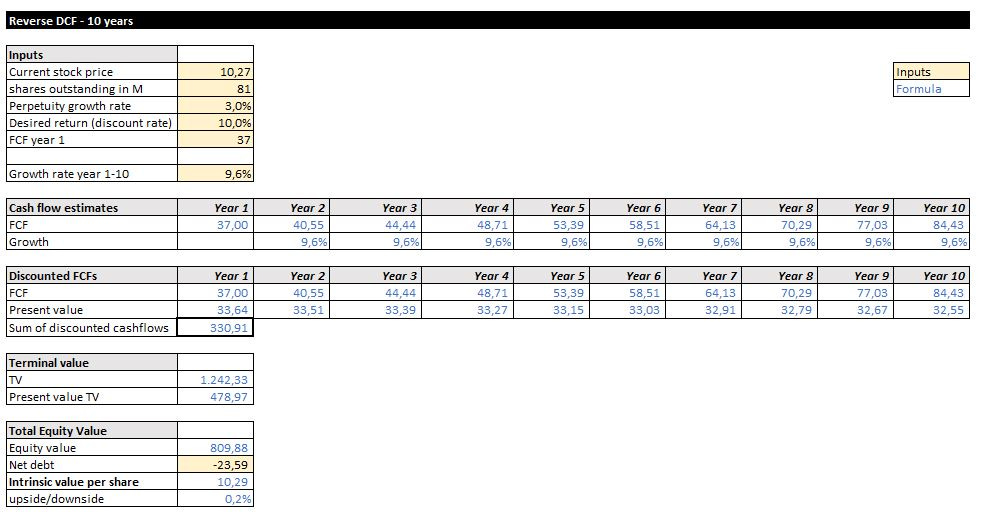

Reverse DCF

Starting with known data points and working backwards to assess market expectations and judge whether these expectations are realistic.

Let’s first have a look at the reverse DCF:

As you can see the company should grow it’s free cash flow by 9.6% annually in order to get a desired return of 10% per year. Given the strategy where the company wants to grow organically and inorganically I expect they will grow closer towards 15% next years given the new strategy is bearing fruit. So it looks like there is a margin of safety at a stock price of 10.27 CAD.

FCF yield

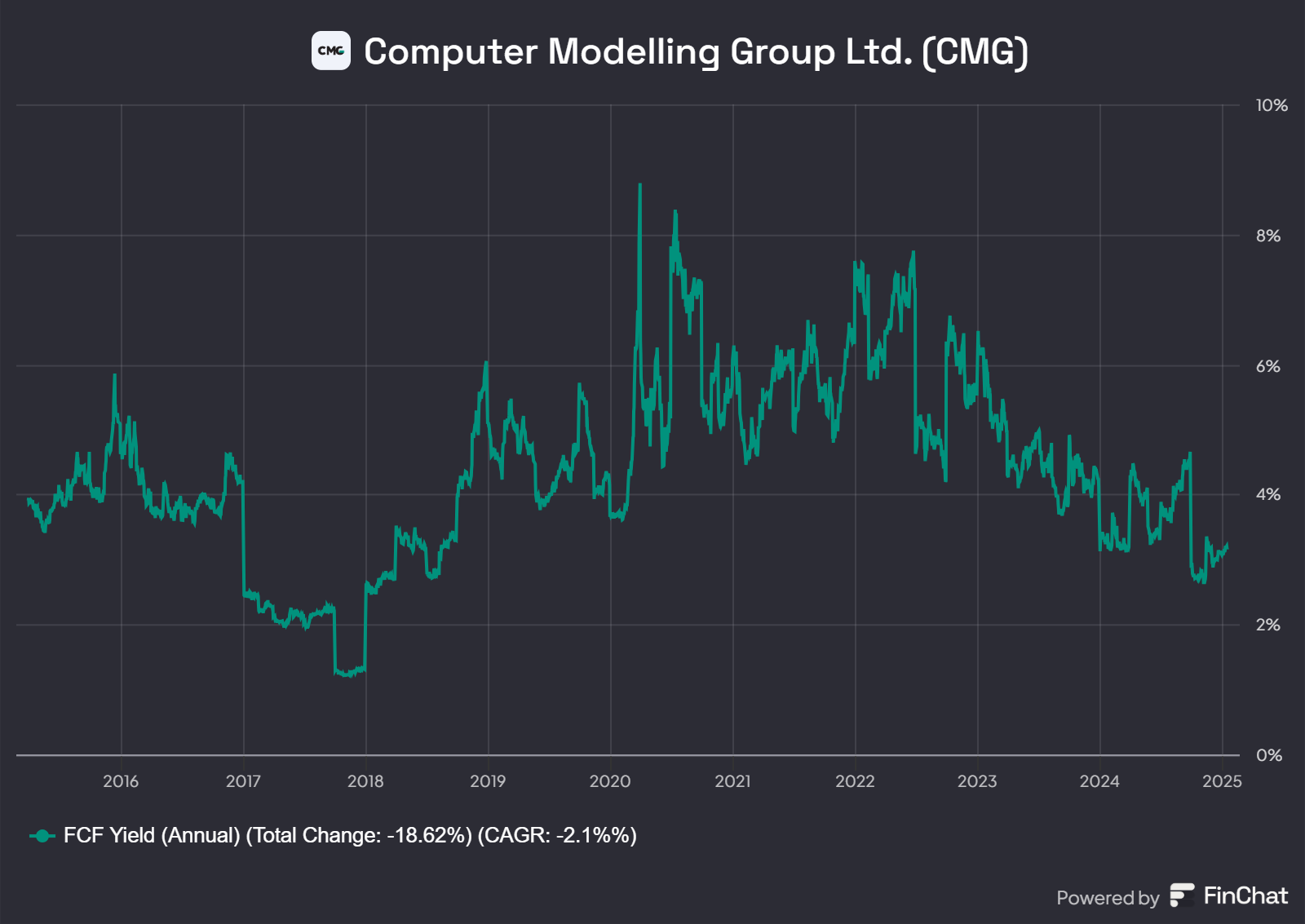

If the Free Cash Flow yield is lower than historical average it might suggest overvaluation. Let’s have a look for CMG.

In 2024 CMG had a cash flow of 35.3M CAD. Based on current market cap of close to 850M CAD, this is 4.2%. This is higher than the FCF yield in the prior years. Below figure shows the FCF yield per year, only for the trailing twelve months the FCF yield looks too low, because of the lower free cash flow in the first half year which is related to the billing of Bluware. Current figure should be the calculated 4.2%.

If CMG can grow it Free Cash Flow for 2025 with 10% towards 38.8M the FCF yield increases towards 4.7%. The average of the FCF yield the last ten years is 4.4%.

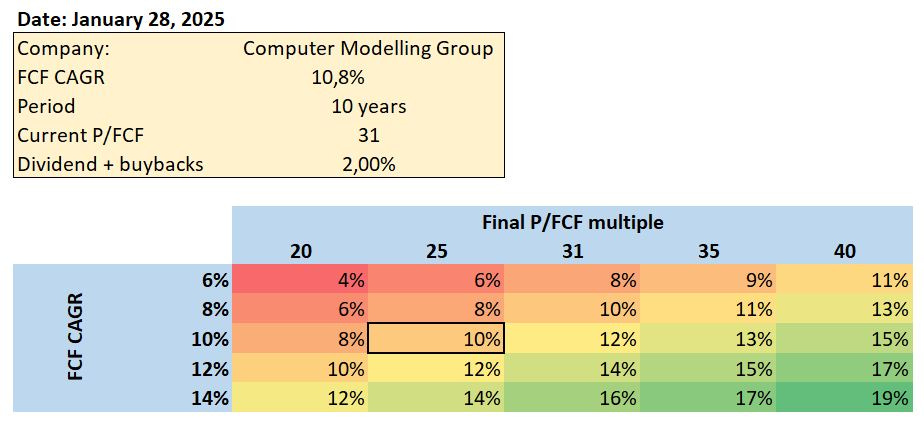

Heatmap

The heatmap for CMG shows the return which one might expect depending on the growth in free cash flow and the growth or decline in the price to cash flow.

For CMG the expected return with a 10% annual growth of the cash flow and a decrease of the Price / Free Cash Flow ratio towards 25 (currently 31) will result in an annual return of 10%. I expect management to do (much) better with their newly announced strategy. First half year revenue increased by plus 38% (6% organic and 32% Bluware acquisition). I expect CMG to get towards 14% free cash flow CAGR or higher, which would result in an annual return of 14%.

Risks

There are several key risks to consider regarding an investment in Computer Modelling Group:

Technological disruptions: As a software and consulting technology company, CMG faces risks related to rapid technological changes and potential disruptions in the industry.

Cybersecurity threats: Given the nature of CMG's business, cybersecurity risks could pose significant threats to the company's operations and reputation.

Regulatory changes: The energy industry, which CMG serves, is subject to evolving regulations that could impact the company's business model and growth strategy.

Economic uncertainties: Fluctuations in the global economy and energy markets could affect CMG's client base and revenue streams.

Execution risks: The success of the CMG 4.0 Strategy depends on effective implementation across multiple growth levers, including core simulation, CoFlow commercialization, energy transition consulting, and strategic partnerships.

Acquisition risks: Part of the CMG 4.0 Strategy involves potential acquisitions, which carry inherent risks such as integration challenges and potential overpayment.

Market competition: As CMG expands into new markets and technologies, it may face increased competition from established players and new entrants.

Talent retention: The success of CMG's consulting practice and software development relies on retaining skilled professionals in a competitive job market.

To mitigate these risks CMG needs to maintain robust risk management practices, diversify its product offerings, implement strong security protocols, and maintain a solid financial position.

Final Conclusion

The quick scan resulted in a perfect score for CMG

a healthy balance sheet with:

a net cash position

a low goodwill balance

a capital-light business model

high cash-conversion

high gross and net margins

Strong management, especially the CEO Mr. Jain who joined in 2022

CMG Strategy 4.0 is all what I’m looking for in a company

Diversified customer base

High NPS score

Runway for growth (Geomodelling and Drilling & Completions)

Attractive valuation, not a bargain though

Reverse DCF shows a market expectation of 9.6% growth a year in free cash flow(revenue growth since 2022 at 28%), which seems low from the half-year earnings

FCF yield around their average

Heatmap: 14% annual return at a 14% free cash flow CAGR

Mitigation of risks is manageable

Conclusion: CMG’s strategy, high-level management, high NPS and sticky software are all I’m looking for. It could have been better is the company was led by the founder and the CEO had a higher ownership in the company. But you can’t have it all!

Hopefully you have enjoyed this deep dive. Feel free to like the post and share it with friends!

Disclaimer

The information in this article is provided for informational and educational purposes only.

The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions.

Great write up! In the recent report was mentioned that the largest customer comprised 25% of total revenue. And that R&P revenue declined due to customer attrition. Any thoughts on these findings?

Wonderful job Arnold!