Nu Holdings: Revolutionizing Banking in Latin America

A Deep Dive into the Digital Disruptor's Growth, Moats, and Future Potential - Nu Bank Stock Analysis 2025

Welcome to Compound & Fire, where we’re on a mission to build wealth the smart way, hunting for top-quality businesses that grow shareholder value over the long haul, paving the road to financial freedom and early retirement.

This community is free, but if you’re enjoying the deep dives and want to fuel more, you can treat me to a coffee on Buy Me a Coffee. Or actually, in this case buy Steven a coffee. A special thanks to Steven van der Burg, an invaluable member of our Compound & Fire community, for doing this amazing work on this deep dive. Give him a follow on X and join the conversation in our Global Quality Investing Discord App where you can find Steven and 500 other quality investing enthusiasts!

Introduction

My Quick Scan recently evaluated NU Holdings, a leading digital banking platform founded in Brazil in 2013 by David Vélez (Colombia), Cristina Junqueira (Brazil), and Adam Edward Wible (USA). The quick scan assigned an Investment Readiness Score of 90.3, signaling a company worthy of a detailed deep dive.

The company began by offering a no-fee credit card managed entirely via a mobile app, which was a disruptive response to Brazil’s fee-heavy, bureaucratic banking system. Over time, Nubank expanded into a comprehensive suite of financial services, including savings accounts, personal loans, insurance brokerage, investments, and even non-financial offerings like a travel booking platform (NuTravel) and a mobile phone service (NuCel).

The company went public on the NYSE in December 2021 at a valuation of USD 45 billion (IPO price USD 9 per share), making it one of the most valuable financial institutions in Latin America. Notably, Nubank raised this capital at the peak of a tech boom, fortifying its balance sheet ahead of a more challenging macroeconomic turn in 2022.

This deep dive article will cover Nu Holdings management, their culture, it’s product and services, business model, strategy and moats, competition, growth expectations and valuation and will include a buy-below price and the final score. Let us know whether you liked this extended deep dive!

Management

David Vélez – Co-Founder, CEO & Chairman (Age:41)

David Vélez Osorno is Nubank’s chief architect and leader. A Colombian by birth, Vélez had first-hand frustration with Latin American banking when he tried to open a bank account in Brazil, an experience of bureaucratic hurdles and high fees that inspired Nubank’s founding. Before starting Nubank in 2013, Vélez was a successful venture capitalist: he was a partner at Sequoia Capital (2011 – 2013) in charge of LatAm investments. He also worked in investment banking and growth equity at Goldman Sachs, Morgan Stanley, and General Atlantic. He holds a BS in Management Science & Engineering and an MBA from Stanford University, giving him both analytical and business skills.

Source: 2Q25 Earnings Release

As Nubank’s CEO, Vélez is widely regarded as a visionary, customer-obsessed leader who grew the company from a small startup to a NYSE-listed banking giant in under a decade. He is known for championing Nubank’s fanatical focus on customer experience and its nonconformist, tech-driven culture. Vélez also serves as Chairman of the Board, cementing his influence over Nubank’s strategic direction.

He has skin in the game: Vélez is Nubank’s largest shareholder. As of the IPO, he owned 938 million shares, mostly Class B with 20× voting power, giving him 75% of voting rights and 19% of economic ownership.

Vélez’s continued leadership is viewed as a key asset. If he were to depart, it could be destabilizing. However, he’s relatively young and deeply committed to Nubank’s mission, so this risk seems low. Overall, Vélez’s mix of venture capital mindset, regional knowledge, and tech vision has been instrumental in Nubank’s rise. He has stated goals as bold as making Nubank ‘the most valuable bank in the world’ and maintaining the company’s culture at scale. Thus far, he has shown prudent decision-making and an ability to attract top talent to the team.

Cristina Junqueira – Co-Founder & Chief Growth Officer (Age 41)

Cristina Junqueira is Nubank’s prominent co-founder alongside Vélez. A Brazilian native, she worked at Itaú Unibanco in credit cards and consumer lending prior to Nubank. She has an engineering background and an MBA from Kellogg. At Nubank’s inception, Junqueira brought deep knowledge of Brazil’s banking products and customer pain points, having seen it from the inside at Itaú. She was instrumental in designing Nubank’s initial credit card product and customer support ethos. She famously insisted on no fine print or hidden fees. For many years, Junqueira was Nubank’s public face in Brazil and led its marketing and growth efforts.

In 2022, her role formalized as Chief Growth Officer (CGO) for the group. In this capacity, she is responsible for growth strategy and operations in new markets (Mexico, Colombia), as well as global marketing and communications. Essentially, she spearheads Nubank’s international expansion playbook and ensures the brand replicates its success outside Brazil.

Junqueira is also a champion of Nubank’s culture and diversity initiatives. She is one of the few female co-founders in fintech and has been recognized in Fortune’s Most Powerful Women International list. She holds a significant equity stake in Nubank as well, about USD 1.8 billion worth as of mid-2025, which amounts to roughly 3% of the company. This makes her one of Brazil’s wealthiest women on paper and aligns her interests with long-term success. Cristina is known to be very customer-centric and detail-oriented, often reviewing customer feedback and instilling Nubank’s fanatical customer love culture in new hires.

Having a co-founder lead growth signals how critical expansion is to Nubank, ensuring new markets getting the same DNA. Her experience at an incumbent bank also provides an insider perspective on how to outmaneuver them. As Brazil CEO until recently, she oversaw Nubank’s core market scaling. Livia Chanes took over the Brazil CEO role in 2024 so that Cristina can focus fully on growth dimensions. These include cross selling more products per customer and pushing into new geographies.

Guilherme Marques do Lago – Chief Financial Officer (Age 45)

Guilherme do Lago has been Nubank’s CFO since Feb 2021. He joined Nubank in 2019 as VP of Finance and was promoted to CFO two years later. Do Lago brings deep banking and finance experience: he spent 13 years at Credit Suisse (2006 - 2019) in various roles, including Managing Director in the investment banking division. He also had a stint at McKinsey & Co. as a consultant (2005 - 2006). He holds an engineering degree from USP and an MBA from Harvard. As CFO, do Lago oversees Nubank’s financial strategy, accounting, and investor relations.

Colleagues describe him as financially disciplined and detail-oriented, which is evidenced by Nubank’s solid financial disclosures and moves like early securitizations of loan portfolios to manage risk. In 2022, CFO do Lago and Vélez took decisive steps to improve profitability: for example, terminating a 2021 employee share award program (saving USD 70 million per year), and slowing hiring growth. This signals a focus on efficiency and shareholder value from the finance side.

Do Lago’s background at a major global bank likely helps Nubank in dealing with regulators, capital markets, he would have been key in the IPO process, and implementing robust financial controls.

In sum, as CFO he brings a conservative counterweight to Nubank’s rapid expansion, ensuring capital adequacy by holding double the required capital and prudent provisioning. He, along with the CEO, signed off on no near-term dividends and reinvestment of profits, indicating alignment with long-term growth.

Youssef Lahrech – President & Chief Operating Officer (Age 50)

Youssef Lahrech joined Nubank in 2020 as COO and was elevated to President in Aug 2022. He comes with nearly two decades at Capital One in North America. At Capital One (a pioneer in data-driven consumer credit), Lahrech held roles spanning product, analytics, risk, and technology, helping build card and lending businesses in the US and Canada. He has advanced degrees in Mathematics / Engineering from top French schools and MIT, giving him a strong quantitative and technical foundation.

At Nubank, Lahrech reports directly to the CEO and is responsible for day-to-day operations: he oversees product performance, platform reliability, marketing execution, and country operations, as well as corporate support functions. Essentially, while Vélez sets vision, Lahrech drives execution. His experience at Capital One likely informs Nubank’s credit underwriting and use of machine learning. Capital One was famous for its analytical rigor, which aligns with Nubank’s data-driven approach to extending credit to new segments.

Since taking on the President role, Lahrech also coordinates Nubank’s multi-country expansion and cross-functional integration. Insiders credit him with improving Nubank’s operational efficiency. He streamlined processes as Nubank scaled from startup to an 8,000+ employee company. Lahrech’s presence is also a signal to investors that Nubank has seasoned management beyond the founders, capable of running a large, regulated institution. He complements the team by having big-bank operational experience but also the adaptive mindset from Capital One’s innovative culture.

Henrique Camossa Fragelli – Chief Risk Officer (CRO)

A seasoned risk manager, CRO since 2018. He has global risk experience at HSBC London. Fragelli is responsible for all risk disciplines such as credit, market, liquidity, operational and AML. His leadership has been crucial in keeping Nubank’s credit losses relatively low and ensuring regulatory compliance as the company grew. He brings a conservative risk culture to balance Nubank’s rapid growth.

Jagpreet Duggal – Chief Product Officer (CPO)

Joined 2020, previously at Facebook and Google. He leads product strategy and development. Under his watch Nubank launched dozens of new features. His Silicon Valley experience reinforces Nubank’s tech/product excellence.

Thuan Pham – Chief Technology Officer (CTO)

Ex-CTO of Uber, joined Nubank in 2022. With Pham’s addition, Nubank gained one of the world’s top engineering leaders, ensuring its platform scales globally.

Livia Chanes – Brazil CEO (since Jan 2024)

Livia was promoted to handle day-to-day in Brazil. She’s ex-Itaú and ex-McKinsey and highly experienced in digital products. Her appointment allows Junqueira to focus on group growth, and brings specialized leadership to Nubank’s largest market.

Are incentives aligned?

Nubank’s approach to capital allocation has been characterized by aggressive reinvestment for growth, careful attention to maintaining a strong capital base, and gradually increasing focus on profitability metrics like Return On Equity (ROE).

Nubank has not paid any dividends and does not plan to in the near term. All earnings are plowed back into expanding the business, be it launching new products, marketing to acquire customers, or geographic expansion. Similarly, Nubank has not engaged in share buybacks; any excess capital is seen as fuel for growth rather than to be returned. Management explicitly states that given the high growth opportunities and high returns on invested capital internally, retaining earnings is the best use. This aligns with shareholder interests as I expect Nubank can continue to earn high ROE levels on reinvested funds.

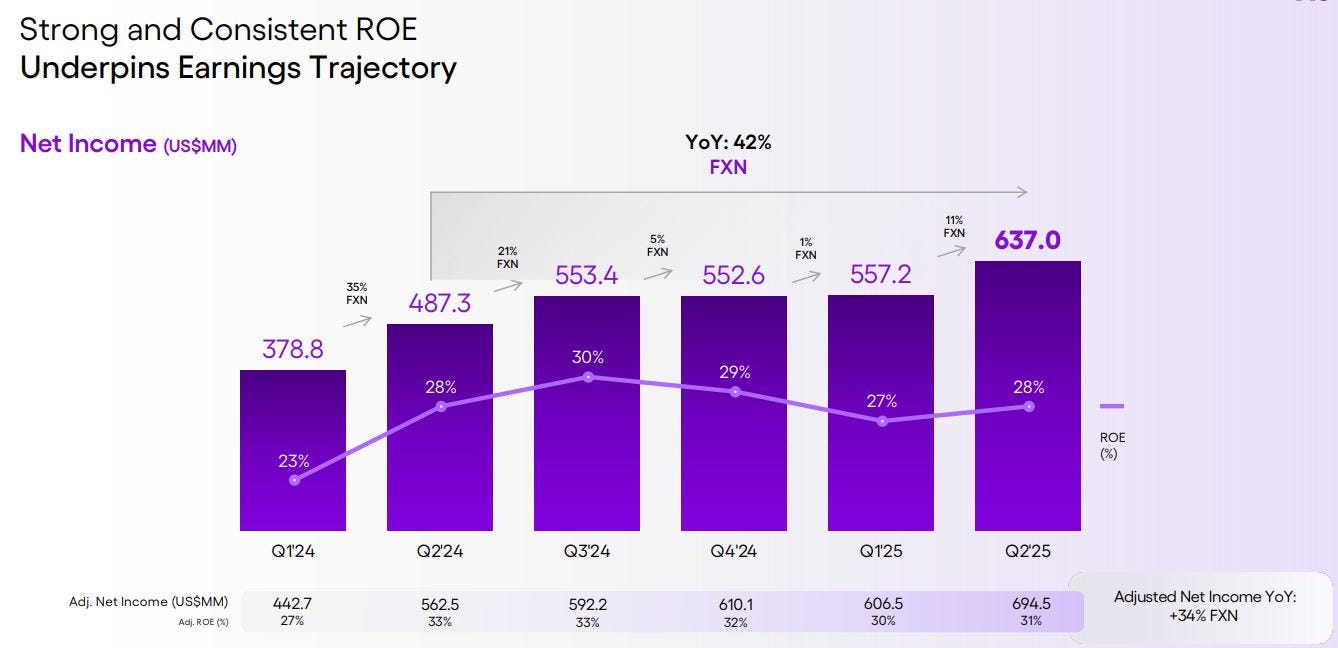

Decent ROE

Early on, as a fintech, Nubank prioritized growth over immediate profitability along with venture backing to subsidize acquisition. However, as a public company, it has started demonstrating a strong focus on improving ROE and efficiency. In 2024 and 2025, Nubank delivered a 28% - 30% ROE, which is far above peers. Nubank’s capital adequacy is strong by roughly 2× regulatory minimum, but not grossly overcapitalized to depress ROE.

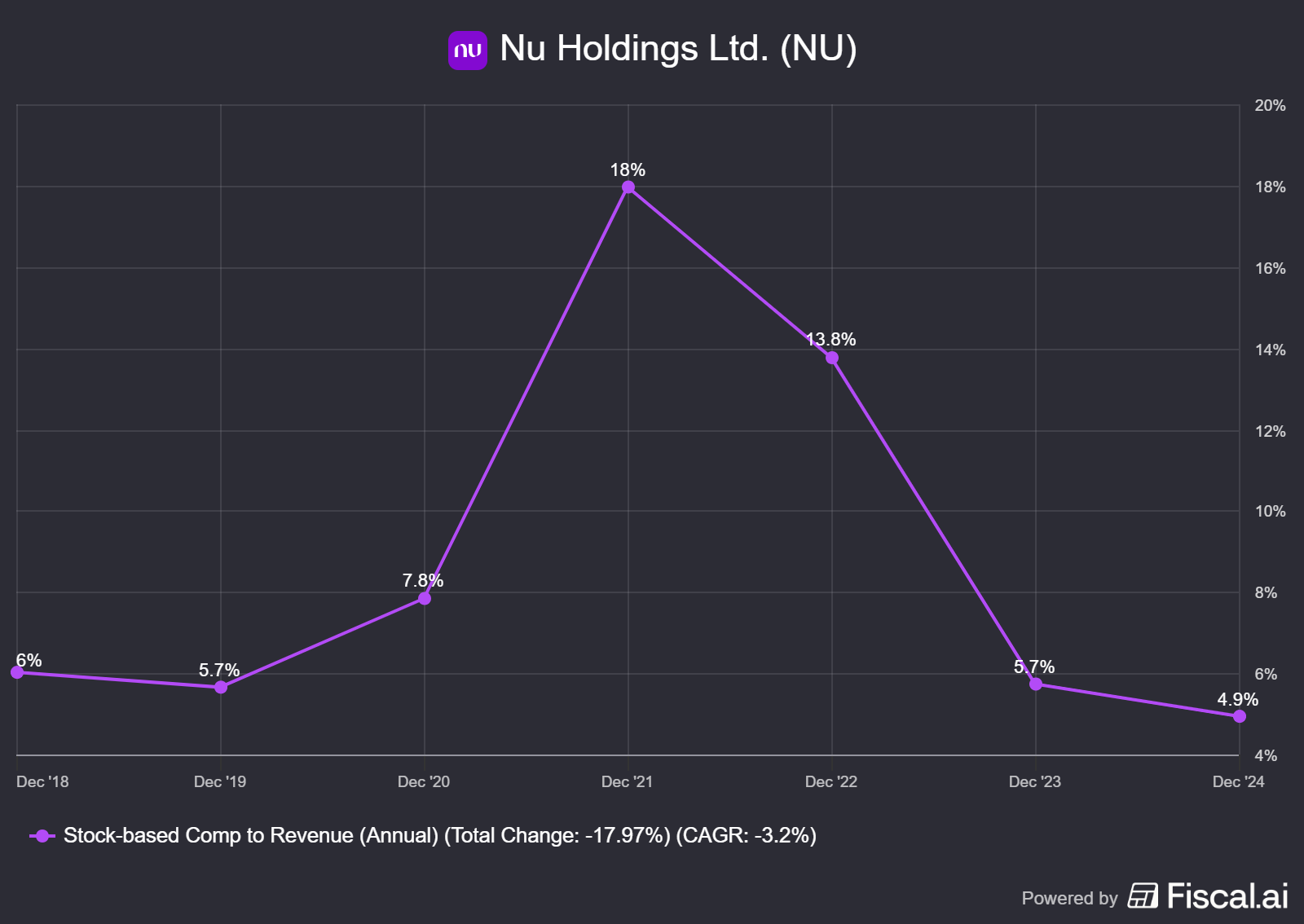

Yes, there is Stock-Based Compensation, but reasonable for a fintech

Like many tech firms, Nubank has used SBC to attract talent. This leads to dilution, which shareholders watch carefully. Nubank had relatively high SBC as a percentage of revenue and currently it hovers around 4.8%. Management has indicated SBC as a percent of revenue will come down as the company scales.

In 2022, Nubank took a notable step by canceling a large contingent share award program from 2021. CEO Vélez himself agreed to terminate that program early, forfeiting some of his own potential awards, to eliminate USD 70 million in annual expense and corresponding dilution. This was a shareholder-friendly move showing management’s willingness to contain dilution and improve per-share metrics.

Due to their SBC program, 76% of employees held shares or awards as of December 2021 (IPO), which is positive for shareholder alignment.

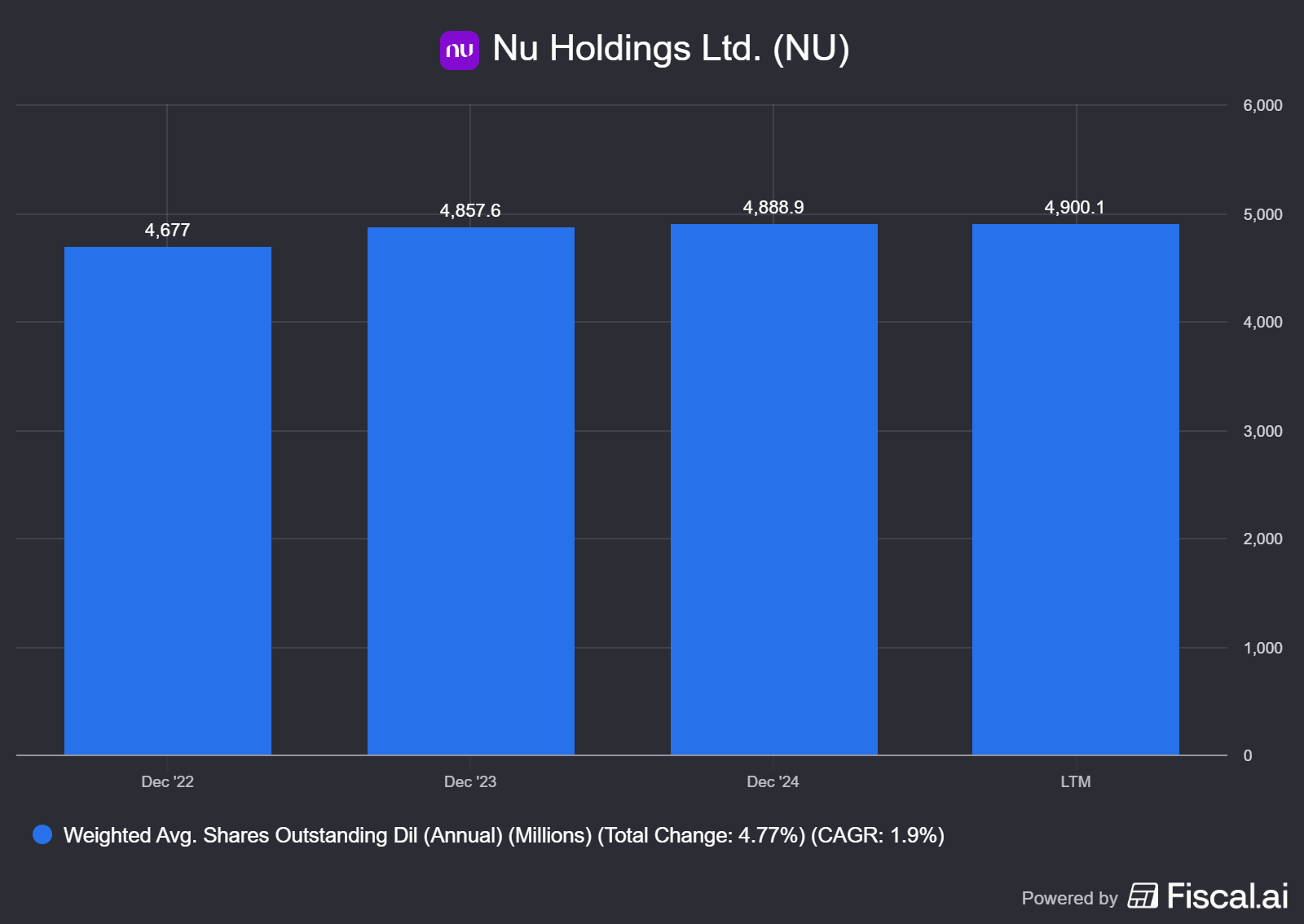

Nubank’s share count did increase post-IPO due to employee options / RSUs vesting, but at a measured pace. As of end-2024, Class A + Class B shares outstanding were ca. 4.9 billion, up only slightly from 4.7 billion at end-2022.

Use of IPO proceeds

Nubank raised $2.6 billion in its IPO in late 2021. Management essentially pre-funded a lot of growth with that money. They haven’t squandered it; rather, it allowed them to comply with higher capital needs for a growing loan book and to expand safely through the 2022 high-rate period without needing to raise costly debt or dilutive equity at lower valuations. This shows good timing and foresight in capital raising. They also secured additional credit lines of USD 650 million in 2022 as backup liquidity. So capital allocation has been prudent in terms of ensuring ample liquidity but not lazily sitting on cash, Nubank’s cash and investments are largely utilized to fund credit growth.

No value-destroying acquisitions - so far

Nubank has made some acquisitions (Easynvest in 2020 for investments, an engineering firm, etc.), but these have been strategic and relatively small. Easynvest was a partly stock deal of USD 70 million. Management hasn’t attempted any oversized, unrelated M&A that would risk capital. All moves like acquiring a minority stake in an Indian payments firm or small tech tuck-ins have been to augment capabilities. Nubank’s management seems inclined to grow mostly organically and only buy if it accelerates their roadmap. Easynvest gave them a brokerage license and 1.5 million clients instantly.

Is Management Transparent?

Nubank’s shareholder communications have been regarded as quite thorough for a young company. The 2022 report even had a ‘Dear shareholder’ letter by Vélez with candid reflections on the year. The annual letters provide detailed metrics like ARPAC, cost-to-serve, activity rate, primary bank NPS, etc., which many banks do not disclose. This level of transparency builds trust that management is not hiding issues.

Solid external reputation

Nubank has earned significant third-party recognition for its transparency and corporate reputation. It’s been named the #1 strongest brand in Brazil in 2023 and won dozens of awards including ones for customer service and innovation. Such accolades imply that not only customers but also industry observers see Nubank as a trustworthy, well-run company.

Culture

Nubank’s culture is a mission-driven blend of customer obsession, innovation, diversity, ownership, and efficiency, designed to empower both users and employees in Latin America’s financial landscape. Their customer-first ethos stands out and fights complexity to deliver "memorable customer experiences."

This culture has been instrumental in attracting top talent both locally and globally, growing to approximately 9,000 employees by 2023 (from 6,000 in 2021) while maintaining a high talent bar. The company has hired senior leaders from world-class firms, such as a former Uber CTO and ex-Facebook product managers, a rarity for a Latin American company, showcasing its ability to compete on a global stage.

Glassdoor reviews reinforce this, with a 4.4/5 overall rating and 91% of employees recommending Nubank, indicating strong employee satisfaction. Reviews frequently praise the mission-driven work and innovative leadership, which aligns with the founders’ emphasis on challenging the status quo through first-principles thinking.

Nubank’s culture encourages bold innovation, building a digitally-native, cloud-based platform with full ownership of its technology stack, enabling control over its destiny. Employees are empowered to act as "protagonists" in a low-ego, mistake-tolerant environment where learning is prioritized: "making mistakes and learning from them is actively encouraged."

The company’s commitment to diversity is another pillar, with the founders highlighting the importance of "strong and diverse teams" to drive creativity and problem-solving. Hiring the "best and most talented people regardless of their CV or pedigree" creates an inclusive workplace that attracts global talent, fostering a meritocratic culture where employees think and act like owners, not renters.

Nubank’s management consciously nurtures this culture, maintaining a relatively flat structure initially and empowering small, autonomous teams dubbed "mini startups." This structure encourages ownership and accountability, with zero tolerance for status symbols or ego, as the founders note: "there is no ego." Despite scaling rapidly, retention remains strong, with key executives staying, suggesting success in preserving this culture.

Are they able to adapt quickly?

Nubank’s culture of ‘challenge the status quo’ inherently means being adaptive. We saw adaptability in product pivots. When customers asked for a loyalty program, Nubank built NuRewards. When Pix emerged, Nubank integrated it deeply, even though it disrupts some card usage.

When the pandemic hit, Nubank quickly moved to remote work and still kept productivity high. The company’s quick expansions into new verticals shows willingness to pivot and experiment beyond core banking. Launching a mobile MVNO (NuCel) is non-traditional for a bank, but Nubank saw an opportunity to keep customers engaged in their app ecosystem with a telco offering. This cross-industry pivot indicates a fearless, agile culture set by management.

Do they have a healthy risk governance framework?

An important aspect of culture in a bank is risk management culture. Nubank’s management has instilled a modern, quantitative risk culture and simultaneously a cautious lending approach despite appearances. For example, they often started customers with low credit limits to learn behavior, then gradually increased. This is a cultural decision to prefer safe growth in credit vs. aggressive lending for short-term gains. Their CRO’s background and early hiring indicates they built robust risk frameworks early. By 2018 they had a CRO and risk team even while private. They maintain a culture where risk concerns can be raised. That shows a healthy balance in culture between growth ambition and decent risk oversight.

Products and Services

Nubank offers several products or services. What started with a credit card offering has been extended with a full platform of financial products, for both consumers and business owners (SME’s). Over time, customers tend to adopt more of Nubank’s financial products, further boosting their overall engagement and the revenue generated per customer. Let’s dive into all these different products, their key features, success to date and recent developments.

Nubank Credit Cards

Nubank’s flagship product is its Nu credit card, a no-annual-fee Mastercard launched in Brazil in 2014. It functions as both a credit and prepaid card with a fully digital experience. Customers can apply and manage everything via the mobile app, including credit limit adjustments, blocking/unblocking the card, and bill payments.

Key Features

No annual fees or maintenance charges, breaking from traditional bank card fees.

Provides digital wallet integration by supporting Apple Pay, Google/Android Pay, and even WhatsApp payments (for the prepaid mode) for convenient contactless use.

Mastercard backing means global acceptance at over 150 million merchants worldwide.

The app offers granular control: real-time spend alerts, instant card locking / unlocking, due date management, and even disposable virtual card numbers for secure one-time purchases.

Unique options like installment discounts for early repayment and investment-backed credit limits, where customers can pledge investments to increase their credit line, enhance flexibility.

For small business owners, Nubank extended this model. Nu Business credit cards offer entrepreneurs the same no-fee, app-managed card benefits, with added ability to transfer limit between personal and business cards for flexibility.

Success to date

Nubank’s credit card pioneered a transparent, customer-friendly approach in Latin America. The absence of fees and the 100% digital onboarding were revolutionary in Brazil’s card market, providing many users their first-ever credit access. By 2024 Nubank reached over 60 million unique credit card customers in Brazil, about 34% of the 14+ population, indicating massive inclusion of first-time cardholders. It holds about 15% of total credit card purchase volume market share in 2024.

A similar impact is seen in Mexico: Nubank launched in 2019 and rapidly became the country’s leading card issuer by 2024 with 5.6 million Mexican card customers, 50% of whom had never had a credit card before Nu. It controls a 5% share of Mexican card purchase volumes by 2024.

This product’s success is measured not only in customer count but also engagement: Nubank cardholders show very high activity rates, which in turn drive fee income (interchange, interest) for the company.

Recent developments

Nubank has continuously enhanced its credit card offering. In recent years it introduced a suite of ‘transaction financing’ features that augment credit card functionality, for example, customers can split an existing purchase into installments after the fact (Purchase Financing), pay utility bills or rent via card and installment (Boleto Financing), or even send instant Pix transfers using their credit line (Pix Financing). These features, all manageable in-app with transparent simulations, effectively turn the credit card into a multi-purpose credit line, boosting interest-earning receivables and customer stickiness.

Nubank also rolled out contactless payment support and digital wallets integration early, and in 2023 it launched Nubank+ and Ultraviolet tiers which build loyalty through cashback and perks tied to card usage.

On the SME side, Nubank added the ability for business owners to request additional corporate cards and enabled Apple Tap-to-Pay on iPhones, turning phones into POS terminals for card acceptance.

Nubank Digital Accounts - NuConta and Cuenta Nu

Nubank offers a fully digital bank account that serves as a checking and savings hybrid. In Brazil this began as the ‘NuConta’ in 2017, and in Mexico and Colombia it is called ‘Cuenta Nu’. The core functions include holding deposits, making transfers and payments, and earning daily interest on balances.

Key features

There are no monthly fees or minimum balance, a stark contrast to traditional banks’ checking accounts.

Idle balances are automatically invested in Brazilian government bonds or time deposits, yielding 100% of the Brazilian interbank rate (CDI) with instant liquidity. Similarly in Mexico, Cuenta Nu offers a very attractive savings APR (around 13% at launch, far above market averages).

Customers enjoy unlimited free peer-to-peer transfers and bill payments, including Pix instant payments in Brazil, at no charge.

A complimentary contactless debit card is provided for ATM withdrawals and purchases from the account balance.

The app includes a ‘Payments Assistant’ to organize recurring bills and reminders, ability to set aside money in ‘Reserves’ or sub-accounts for budgeting goals, and an option to lock funds as a time deposit for higher yield. Customers can also schedule automatic savings contributions to instill good habits.

Success to date

Nubank’s account stands out for its simplicity and generous terms. By eliminating fees and offering interest on all deposits, it attracted customers who were frustrated with legacy banks. The ease of opening an account digitally in minutes (using just an app and an ID) brought many unbanked or underbanked individuals into the financial system.

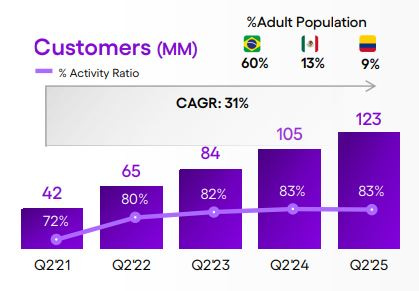

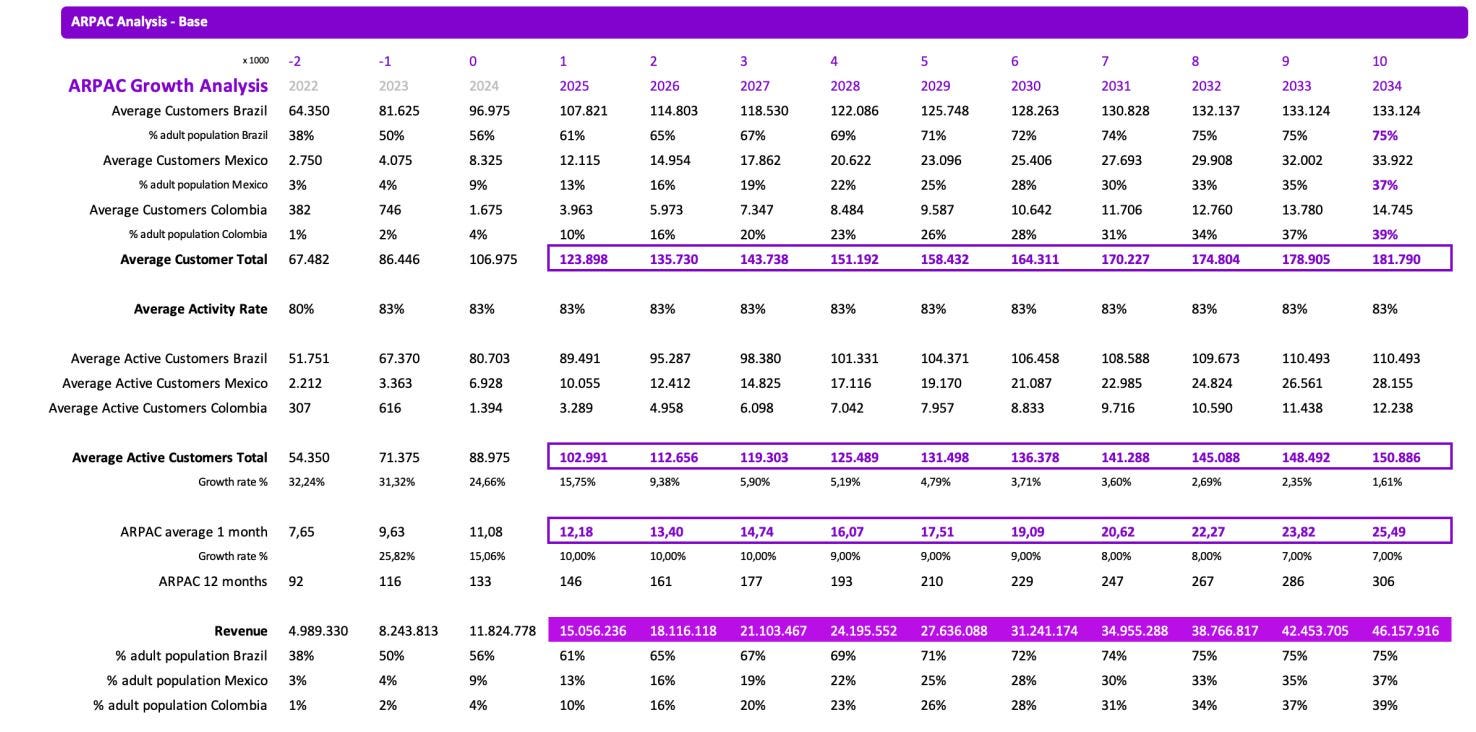

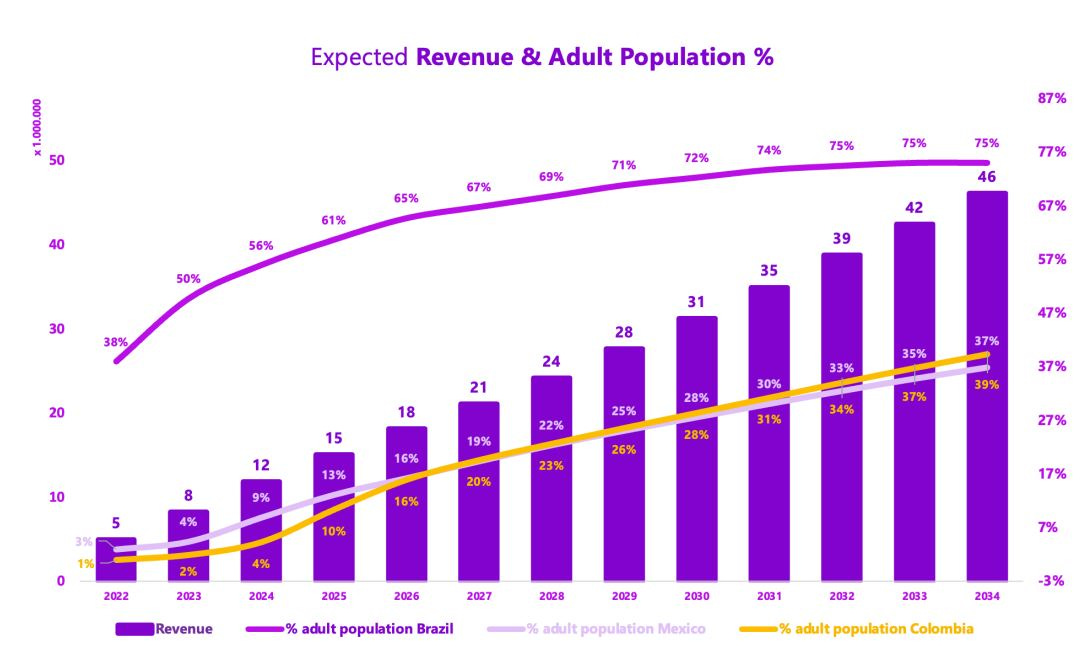

In Brazil, NuConta launched in 2017, rapidly scaling as a free alternative to bank accounts. By Q2 2025, Nubank Brazil had over 107 million customers, many of whom use the account, representing 60% of Brazil’s adult population. Deposits reached USD 36.6 billion by mid-2025, reflecting strong trust in Nubank as a primary bank.

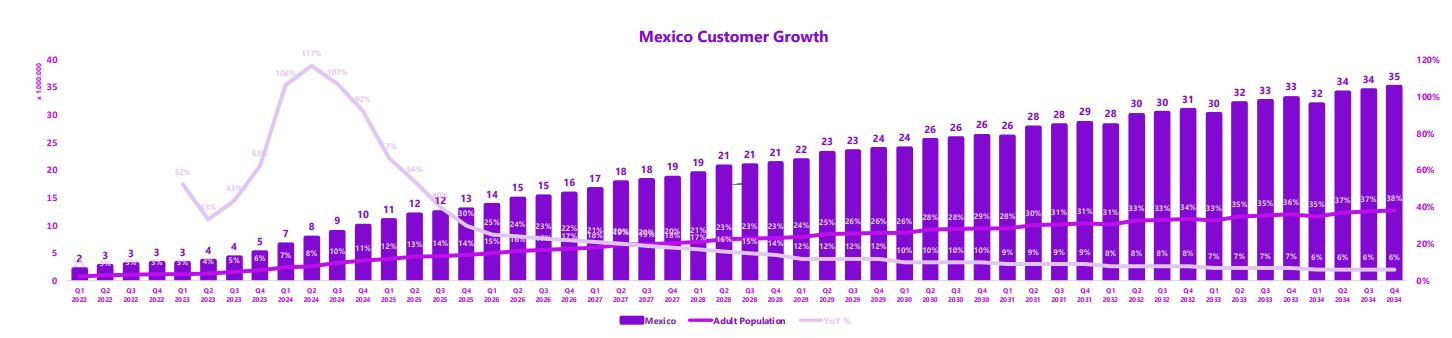

In Mexico, Cuenta Nu was introduced publicly in May 2023 and saw explosive uptake, it reached 1 million accounts in its first month and helped propel Nu Mexico to 10 million customers by the end of 2024. The launch of Cuenta Nu was highly disruptive because it offered an 13% annual yield vs. <1% at incumbents, with 24/7 access and no minimums. By 18 months post-launch, Nu Mexico had USD 3.8 billion in deposits, indicating that a large share of Mexican users adopted the account product. The availability of ‘Cajitas’, money boxes; a savings goal feature, has been cited as a decisive factor for many Mexicans joining Nu.

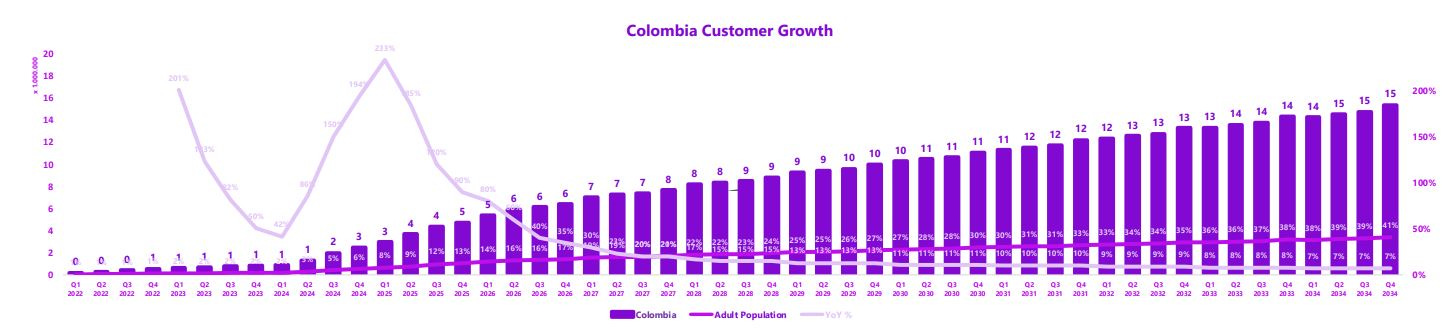

Nu Colombia launched its savings account Cuenta Nu in mid-2024, and this immediately boosted customer growth; Colombia’s base nearly tripled to almost 3 million by early 2025 after the account launch.

The interoperability with each country’s payment infrastructure (Pix in Brazil, SPEI in Mexico, etc.) and the seamless integration with Nubank’s other products (one app for card, account, loans, etc.) provide a one-stop financial hub that is a key selling point.

Overall, Nubank’s accounts have been highly successful: internal data shows over 83% activity rate of customers and surveys in Brazil indicate a large portion of customers consider Nubank their primary financial account.

Recent developments

Nubank has also built a large physical cash network through partnerships, for example, in Mexico it partnered with OXXO stores (30,000+ locations) so that customers can deposit or withdraw cash to their digital accounts easily.

Other recent enhancements include remittances: in 2024, Nu Mexico launched a feature in collaboration with Wise, enabling customers to receive money from the U.S. via WhatsApp.

Nubank Brazil added ‘Locked Deposits’ options, allowing customers to lock a portion of funds for a higher yield. These locked funds can serve as collateral for credit products.

The account’s payment capabilities have also grown: Nubank was among the first to support Pix instant payments since its 2020 debut, and has added Pix keys, QR code payments, and even voice-initiated Pix via WhatsApp. All these updates keep Nubank’s account on par or ahead of competitors in features.

On the SME side, Nubank’s business account has seen new tools like ‘Meus Impostos MEI’ – an in-app tax module to generate and pay monthly tax forms for solo entrepreneurs, reducing bureaucracy for business owners.

A confirmed near-term development in Mexico; having secured a full banking license in April 2025, Nu plans to introduce payroll accounts and other enhanced deposit products. A payroll account would allow Mexican customers to have their salaries deposited directly into Nubank, likely with perks or interest incentives to capture paychecks from traditional banks.

Nubank Personal Lending – Unsecured and Secured

Nubank offers a range of lending solutions, from unsecured personal loans to new secured loan types, all delivered digitally. Personal Unsecured Loans are simple cash loans available to pre-approved Nubank customers through the app. Borrowers can simulate different loan amounts and terms, accept an offer instantly, and receive the money directly into their Nu account within seconds.

Key features

From simulation to approval to disbursement, everything happens in-app in real time. There’s no paperwork or branch visit, aligning with Nubank’s digital model.

The app provides transparent sliders to adjust loan amount and tenure and see the resulting interest and installment clearly. After taking a loan, customers can manage it easily. They can prepay installments or the full loan at any time through the app, often with a discount for early payoff.

In Brazil, Nubank’s personal loan interest rates are below market average for equivalent profiles, thanks to efficient underwriting and lower overhead. The terms are clearly disclosed with no hidden fees.

Loan funds are deposited instantly into the customer’s Nubank account, making access to cash seamless. Repayments can likewise be auto debited, simplifying the experience.

Beyond unsecured loans, Nubank has introduced Secured lending products in Brazil, split up in the following variants:

Investment-backed Loans: Launched in 2022, this allows customers to borrow against their own investments held with Nubank - such as fixed deposits or government bonds - as collateral. Because of the collateral, customers can get a larger credit line at a lower interest rate than an unsecured loan. Crucially, the borrower’s investments stay intact and continue earning, allowing them to handle short-term cash needs without liquidating assets.

Payroll-Deductible Loans ‘Consignado’: Introduced in 2023, this is a form of secured loan where repayment is guaranteed by automatic payroll deduction. Nubank partnered with Brazil’s largest public payroll systems, covering federal employees, military, and pensioners, to offer these loans, which carry very low interest rates. The automation removes the need for intermediaries or brokers.

FGTS-Backed Loans: Also launched in 2023, these loans let customers borrow against their FGTS - a Brazilian severance fund, annual withdrawal allowance. Essentially, Nubank advances the customer a lump sum, and the government’s FGTS fund repays Nubank annually from the customer’s accrued benefits. This gives people early access to money that is ‘theirs’ in a safe, low-rate manner.

Unique Selling Points

Nubank’s lending products emphasize ease, transparency, and inclusion. A major unique point is how accessible these loans are: because Nubank leverages its vast customer data and AI-driven underwriting, it often extends credit to users who might be overlooked by traditional banks.

In Mexico, for instance, personal loans, launched in 2023, are helping deepen customer relationships in a country where consumer credit is underpenetrated. Nubank’s unsecured loans have no requirement for guarantors or physical documents, removing barriers typical in Latin America.

The secured loans are innovative: the investment-backed loan is uncommon in the region and appeals to more affluent customers as a way to handle emergencies without sacrificing investments. The payroll and FGTS loans differentiate Nubank by entering segments traditionally dominated by public banks and niche lenders; Nubank’s value proposition here is a fully digital, no-hassle process and the lowest price in the market for many customers. By bringing its tech efficiency to secured loans, Nubank’s USP is simplifying what are otherwise bureaucratic products. Payroll loans usually involve lots of paperwork; Nubank makes it a few taps.

Success to date

Nubank’s unsecured personal loans launched in Brazil in 2019, and later in Mexico in 2023 and Colombia in 2024. Take-up has been strong: as of Q1 2025, Nubank’s total loan portfolio reached USD 24.1 billion, up 40% year-on-year.

The secured loans are newer but ramping up: Nubank acquired a 182 million dollar portfolio of third-party payroll loans in Q1 2025 to accelerate entry, and is already working with major government payroll systems, covering 60% of the addressable market.

Nubank SME & Business Banking – Nu Empresas

Nubank has built a strong suite of offerings for small and medium-sized enterprises (SMEs) under its ‘Nu Empresas’ (Nu Business) accounts. These business accounts function much like the personal accounts but tailored for entrepreneurs to manage company finances with ease.

Key features

Entrepreneurs. including sole proprietors (MEI), single-owner LLCs (EIRELI/LTDA), and companies with multiple partners can open a business account entirely via the app in minutes, provided the owners are Nubank individual customers. This 100% digital process was pioneering in Brazil’s business banking.

The business account has no maintenance fees or opening fees, saving businesses significant costs. Transactions like transfers are mostly free, including Pix for enterprises. Nubank was one of the first to waive Pix fees for business users.

Business customers get a debit card for expenses and can make unlimited free payments such as bill pay, employee transfers, taxes, etc.. For receiving money, Nubank provides multiple channels;

free Pix keys to accept instant payments of which 91% of business clients already use Pix to receive payments;

a payment link feature to generate payment URLs for clients;

NuTap, a software that allows merchants to accept card payments on their smartphone - no card reader device needed. Notably, Tap to Pay on iPhone was enabled in early 2024, making iPhones into card terminals with Nubank’s app.

Nubank’s business app includes extras like the calculation and payment of the monthly MEI tax within the app. There’s also a Bills / Payment Assistant to track due dates for the business’s recurring expenses, akin to the personal account feature. Business owners can easily separate personal vs. business finances, with distinct account interfaces under one login.

For credit, Nubank offers a Nu Empresas credit card with no annual fee and similar perks as the personal card. In 2021 Nubank began testing credit cards with businesses and saw enthusiastic uptake. A unique feature is that entrepreneurs can shift part of their personal card limit to their business card if needed, providing flexibility in credit allocation.

In late 2024, Nubank also launched Working Capital loans, its first dedicated SME loan product, offering tailored credit lines to support business cash flow needs.

Additionally, in 2023 it introduced ‘Nu Limite Garantido’ for businesses, allowing companies to increase their credit card limit by posting an investment as collateral.

Unique Selling Points

Nubank’s business banking USP is simplicity and cost savings for entrepreneurs. Traditionally, Brazilian SMEs faced tedious paperwork to open accounts and were often charged high fees for basic services. Nubank turned that on its head by offering a quick, no-bureaucracy signup and zero fees on the account. This directly addresses a ‘latent pain’ of entrepreneurs, as business owners want to focus on their business, not bank bureaucracy or abusive fees.

Another selling point is how feature-rich the Nu business account is despite being free: entrepreneurs get tools like tax payment and free Pix payments that would usually be add-ons elsewhere. The integration of NuTap at competitive transaction fees, Nubank’s merchant fees are 30% lower than typical, is a unique benefit that effectively adds payment acquiring to the account offering.

Nubank also leverages its large base of entrepreneur clients, 10 million of its individual customers are entrepreneurs, to cross-sell. 76% of business users are MEIs (sole proprietors) who likely were Nubank individual users first. The ecosystem allows business owners to seamlessly manage personal and business finances in one app, transferring between them as needed.

This led to high customer satisfaction Nubank’s business service achieved #1 NPS in SME banking in Brazil by H2 2022, indicating strong word-of-mouth.

Success to date

Nubank launched its business accounts around mid-2019, initially to sole proprietors upon heavy customer request. Growth has been remarkable: by June 2023 Nubank had 3 million business customers, up 60% in one year. By early 2024, this reached 4 million business customers. Nubank now likely has the largest SME customer base of any bank in Brazil. Moreover, internal surveys show 58% of active business customers use Nubank as their primary business account, meaning they have moved most of their financial activity to Nubank.

Nubank’s share of the SME market profit pool is still small; <1% of Brazil’s USD 11 billion SME credit profit pool as of 2024. On credit, Nubank’s SME credit card issuance has grown, and in October 2024 Nubank disclosed that 65% of its SME borrowers were getting their first-ever business loan through Nubank. Loan volumes to SMEs grew 150% after launching the Working Capital line. This indicates significant success in extending credit to underserved small businesses.

Nubank Investment - NuInvest

Nubank’s journey into investments began with its 2021 acquisition of Easynvest, an online broker, rebranded as NuInvest. Now, Nubank offers customers an array of investment products integrated into the app, aiming to make investing as easy as spending or saving.

Key features

Customers can invest in stocks, ETFs, mutual funds, Brazilian government bonds (Tesouro Direto), high-yield savings bonds (CDBs), and more – all through the Nubank app. The platform offers a wide portfolio of choices, catering to both conservative savers and more aggressive investors.

Nubank introduced zero-commission stock trading for Brazilian equities, a significant USP as many brokers charge fees. Most investment products have transparent pricing with no hidden management fees by Nubank.

The emphasis is on demystifying investing. The app provides clear, jargon-free information on each product and even personalized recommendations or nudges based on a customer’s profile. Educational content is woven in to help new investors. There is also portfolio tracking so users can monitor performance easily.

Importantly, Nubank integrated investing with banking, transfers between the Nu account and NuInvest are seamless, and some features overlap. Money in the main account is actually auto-invested in a money market by default. This means no complex account setup; a Nubank user can start investing literally with a few taps. The app’s design treats investing goals as an extension of saving.

Unique Selling Points

Nubank’s investment offerings are built around accessibility and integration. A key USP is that even very small investors are welcomed – you can start with as little as BRL 1 (USD 0.20) in certain products like government bonds or even crypto (via NuCrypto, discussed next). This lowers the bar for entry dramatically.

Another USP is contextual advice. Nubank’s platform can suggest products appropriate for the customer’s goals, for instance, suggesting a low-risk investment for an emergency fund caixinha. Unlike incumbent brokers that cater to financially savvy clients, Nubank targets the mass population; its study showed that a large portion of its users had never invested before. The bundling of bank and brokerage means instant funding of investments, no delays or complicated transfers, which is an advantage over standalone investment apps. Nubank also leverages its brand trust, as one of the world’s largest digital banks, customers feel comfortable trying investments on the same app they use for daily finances.

Finally, Nubank’s knack for community-building such as educational content, in-app news, and even gamified challenges sets it apart in making investing less intimidating. The Money Boxes concept is relatively unique among banks in Brazil and serves as a USP. It transforms saving into a goal-driven, even enjoyable experience, as opposed to just shuttling money into a generic account.

Success to date

After the Easynvest acquisition, NuInvest officially launched in 2021, and Nubank gradually integrated it by 2022 so that all customers could activate an ‘Investments’ tab in the app. The uptake has been impressive: by late 2023, Nubank reportedly had over 7 million active investing customers, making it one of the largest investment platforms in Brazil by users.

In Brazil, Nubank quickly became a top distributor of government bonds to individuals, reflecting how many users channel their savings via Nu. The Money Boxes feature was also successful – within months of launch, millions of caixinhas were created, and Nubank expanded it to SME customers in Dec 2023 due to demand.

By Q1 2025, Nubank’s investment revenue, largely commission fees, was still a small fraction of overall revenue but growing. The success is also qualitative: Nubank was named the #1 most innovative company in LatAm in 2023 by Fast Company, largely for its impact on financial inclusion in saving and investing.

Nubank Crypto - NuCrypto

NuCrypto is Nubank’s in-app crypto trading and wallet service, launched in 2022. It allows Nubank customers to buy, sell, and hold cryptocurrencies seamlessly through the Nubank interface.

Key features

Users can start investing in crypto with as little as BRL 1 (USD 0.20), making crypto accessible to virtually anyone. This is a stark difference from traditional exchanges that might have higher minimums.

NuCrypto supports trading in a variety of popular cryptocurrencies. Initially launching with Bitcoin (BTC) and Ethereum (ETH), it expanded to include at least 15 different tokens by 2024, such as Uniswap (UNI), Ripple (XRP), Solana (SOL), Stellar (XLM), Polygon (MATIC), Aave, Chainlink, Avalanche, Litecoin, Polkadot (DOT), and even stablecoins like USDC. This breadth allows users to diversify or explore different crypto projects within the same app.

Unlike some fintech crypto offerings that are closed ecosystems, NuCrypto provides a custodial crypto wallet for each user. Users can withdraw their crypto to an external wallet or deposit crypto from outside into their Nubank wallet. Nubank partnered with Fireblocks for secure custody of assets and to facilitate these transfers safely. This feature gives users more control and aligns with crypto norms of being able to move assets freely.

Customers can trade crypto anytime, including weekends, using their Nubank account balance. Because the Nubank account is linked, buying crypto is instant with a tap, and selling converts back to BRL in the account.

NuCrypto not only offers BRL-to-crypto trades but also introduced crypto-to-crypto swap pairs (e.g., BTC↔ETH, BTC↔USDC) with efficient pricing. To ensure good execution, Nubank sources liquidity from multiple providers and does FX conversion via a licensed partner to tap USD markets when needed. This means Nubank users get competitive 14 rates close to global market prices, an important detail in markets where local crypto liquidity can be thin.

Nubank applies its rigorous KYC processes to NuCrypto, meaning only verified Nubank customers can trade. This mitigates fraud risks and aligns with regulations. The user experience emphasizes security. To authorize a crypto transfer, the user must go through strong authentication.

Unique Selling Points

NuCrypto’s primary USP is that it democratized crypto investing for the average person. Many Latin Americans are curious about crypto but find traditional exchanges daunting or unsafe. With Nubank, a trusted brand, offering crypto in the same app as one’s bank, users gained confidence to try it. The integration means no need to create a separate exchange account, remember new passwords, or deal with unfamiliar interfaces.

Another USP is simplicity and educational framing: Nubank provides explainers and ‘price alert’ feature so users can follow market movements with custom notifications. This helps newbies engage without feeling lost.

By offering a range of coins, including a stablecoin (USDC), Nubank also positions itself as a potential platform for dollarized saving. Nubank found that 1 in 4 new NuCrypto investors chose to buy USDC, effectively using it as a digital dollar saving strategy.

Additionally, Nubank’s approach to compliance by registering the necessary approvals, working with licensed partners for FX and using a reputable custody solution as Fireblocks is a USP in terms of safety.

Success to date

Nubank announced crypto trading in May 2022, and by September 2022 it had rolled out to all Brazilian customers. The uptake was very strong: in about a year, Nubank became one of the largest retail crypto platforms in Brazil. The customer increase is impressive; from 1.3 million users in Q2 2023 to 6.6 million users in Q2 2025.

By July 2023, Nubank launched a pilot of NuCoin, a proprietary crypto token intended as a loyalty/rewards token for customers. NuCoin’s testing phase involved select customers and was aimed at creating engagement as users could earn NuCoins for certain activities.

Nubank also integrated crypto content in its marketing by means of educational blog posts, highlighting how easy it is to buy crypto with Nubank. By offering crypto, Nubank increased its ARPAC; crypto trading generates commissions or spread revenue. While still a small portion of overall revenue, it attracts a segment of customers who might otherwise use external platforms.

Nubank Insurance - NuSeguro

Nubank has entered the insurance market by offering a range of affordable, flexible insurance products through its app, under a unified Nu insurance platform - often in partnership with insurance underwriters. The initial product was Nu Vida (life insurance), and since then Nubank has expanded to cover other areas such as mobile phone insurance, and is exploring home, auto, and other protections.

Key features

From getting a quote to customizing coverage to filing claims, everything is done in-app. The process to purchase insurance is fast, simple, and paperless. For example, a user can get a life insurance quote by answering a few questions in the app and instantly see different coverage options.

Nubank’s policies are highly modular. Customers can choose coverage amounts and add-ons to fit their needs and budget. For instance, in life insurance, one can select different payout amounts, add riders for funeral assistance, etc., all with real-time premium updates. This personalization is designed to avoid overpaying for irrelevant coverage.

Nubank positions its insurance as low-cost and disruptive in pricing. Life insurance premiums start as low as 2 dollar per month for basic coverage. There are no surprise fees, and Nubank often forgoes some traditional broker commissions, passing savings to customers. It clearly shows what each level of coverage costs.

Nubank acts as a broker, partnering with established insurers like Chubb for life and phone insurance. This means policies are backed by major insurers but sold and managed through Nubank’s interface. Nubank earns brokerage revenue while the risk is on the partner, a capital-light model.

A critical part of insurance is claims. Nubank leverages its customer service infrastructure to provide 24/7 support and aims to make filing a claim as easy as a few taps, with minimal paperwork. The idea is to remove the notorious hassle from claims. Users can upload documents or photos in-app for a phone insurance claim and track status in real time.

Unique Selling Points

Nubank’s insurance USP is making insurance approachable and fair for a generation that is skeptical of insurers. By integrating insurance into the same app where users manage money, it’s easier to cross-sell at the right moment, like offering phone insurance when a user spends money to buy a phone. The affordability is a key USP: Nubank explicitly markets that for the price of a coffee, you can insure your phone or life, which is compelling in markets where insurance penetration is low.

Furthermore, flexibility is a key topic. Users can start or cancel coverage anytime without penalty via the app. This no-lock-in, no-bureaucracy approach contrasts with legacy insurers.

Nubank also benefits from its trust and transparency; customers who love Nubank for banking are likely to trust it to not mis-sell insurance, which addresses a traditional pain point of aggressive or confusing insurance sales.

Also, by covering new categories like pet insurance or device insurance, Nubank differentiates with a broad suite all accessible in one place. It’s essentially one of the first one-stop-shops for multiple insurance needs in a fintech app in LatAm.

Success to date

Nubank launched its first insurance product, life insurance, in late 2020 in Brazil. In the first year, it reportedly sold hundreds of thousands of policies, indicating strong uptake. By 2022, Nubank was also offering cell phone insurance and ‘Seguro Família’ (a funeral expense coverage) as add-ons. In 2024, Nubank expanded at least with to different insurance products: life, mobile, home and financial protection.

Nubank’s life insurance likely attracted many first-time insured individuals. They emphasize cases where young customers in their 20s took a life policy, historically a rarity in Brazil, showing Nubank’s reach. Also, because Chubb underwrites, claims have been being paid reliably, which helps build Nubank’s credibility in insurance.

The brokerage revenue from insurance is still a small slice. The insurance profit pool in Brazil is around 5 billion dollar and Nubank’s share is <1%, meaning there’s huge room to grow.

Nubank Other Products - NuPay, NuShop, NuTravel, NuCe

NuPay

NuPay is Nubank’s digital checkout / payment solution launched in 2022. It enables Nubank customers to pay online merchants directly via their Nubank app, with just a few clicks, without needing card details.

For customers, NuPay offers convenience and security. At partner e-commerce sites, instead of entering card info, a user can choose NuPay, approve the payment in their app, and it’s done – eliminating risk of card data theft. It’s a one-click purchase experience.

Customers can pay either using their account balance (debit) or their credit line, and importantly, NuPay allows installment payments up to 24x - even beyond the normal card limit. Nubank essentially extends additional credit for NuPay purchases, boosting customers’ purchasing power.

For merchants, NuPay promises higher conversion rates by simplifying checkout and lower fraud because user authentication is handled by Nubank, a trusted party. It settles to merchants quickly and can support recurring payments for subscription services.

NuPay integrates tightly with Nu’s app and NuShop; within the Nu app’s shopping section, purchases use NuPay by default for a seamless end-to-end experience.

Since launch, NuPay has onboarded many popular merchants, including some big retail chains and digital services in Brazil. Its unique proposition is that no sensitive card info is exchanged, and Nubank can approve transactions internally, leading to near-zero payment processing failure for Nubank users. This makes it a strong USP, especially as e-commerce continues to grow in Latin America.

NuShopping

NuShopping is Nubank’s integrated shopping portal in the app, where users can buy goods and services from partner merchants without leaving the Nubank ecosystem. It curates deals from top e-commerce players: for instance, products from Apple, retailers like Casas Bahia, travel bookings via Hopper, and gift cards via Epay are available.

Nubank negotiates special discounts or cashback for its users on this marketplace. For example, a user might get an extra 5% cashback for buying a phone through NuShopping versus going directly.

Users can complete the entire purchase in-app using NuPay, without needing to register on the merchant’s site or input delivery info repeatedly. Nubank essentially acts as the intermediary, streamlining the checkout.

From electronics to travel tickets, NuShopping aims to cover various needs. It keeps users engaged in the Nubank app even when they’re doing non-banking activities, increasing stickiness.

This marketplace also generates commission income for Nubank, adding to ARPAC.

NuShopping was rolled out around 2021 - 2022 and has expanded since. It taps into the trend of super-apps by embedding commerce into finance. The success is evidenced by high engagement; Nubank often mentions how its customers can shop for major brands inside the app with ease.

NuTravel

Launched in 2024, NuTravel is Nubank’s integrated travel booking service. It allows users to search and book flights, hotels, and other travel services directly in the Nubank app.

Nubank touts that bookings via NuTravel come with guaranteed best prices, likely achieved by partnering with travel aggregators or negotiating rates. This instills confidence that customers aren’t paying more for using a new platform.

In partnership with Wise, Nubank offers a multi-currency account alongside travel booking. Users can exchange BRL to USD, EUR, etc., at low rates and hold foreign currency for travel. This is linked to their Nubank account, making spending abroad easier.

With NuTravel, a customer can plan a trip end-to-end: buy airline tickets, book hotels, and handle forex, all in one app. Expenses can be paid with the Nubank card or account, and possibly in installments, taking advantage of Brazilian habit of installment travel purchases.

The synergy with Nubank’s financial products is strong: customers with Ultraviolet tier get extra travel benefits like lounge access, and presumably, those might integrate with NuTravel for a premium experience.

NuTravel includes innovative perks like offering a free international eSIM for roaming data in certain destinations. This addresses a common travel pain point (expensive roaming), adding value beyond financial services.

NuTravel’s launch indicates Nubank’s ambition to be more than a bank – to be a lifestyle platform for its customers. Early usage has likely been driven by Ultraviolet customers and savvy travelers, but over time it could challenge traditional travel agencies and FX services by convenience.

NuCel

In late 2023, Nubank took a bold step outside traditional finance by launching NuCel, a mobile virtual network operator (MVNO) service in partnership with telecom provider Claro. NuCel essentially offers Nubank-branded mobile phone plans.

NuCel’s plan is designed with simplicity; unlimited calls (local and long-distance) and unlimited WhatsApp (including calls) are included. This mirrors Nubank’s style of removing hassle.

Unique to NuCel, customers get access to an exclusive savings box with 120% of CDI return on up to BRL 10,000 deposit, valid for one year. This means if a customer subscribes to NuCel, they can park up to BRL 10,000 in a special account earning 20% above the usual rate, effectively subsidizing their phone bill via extra interest. This is a clever cross-industry perk only Nubank could offer, blending telco and finance.

Nubank applies its DNA of transparency to mobile service. No hidden charges, easy plan management in-app, and Nubank’s highly rated customer support for any telco issues.

NuCel started with a limited rollout in late 2023 and will expand if successful. It’s quite innovative, very few fintechs globally have ventured into telecom, and Nubank’s approach of tying a high-yield savings incentive to it is novel.

What is their Business Model?

Nubank’s business model is fundamentally that of a digital-first bank with a freemium pricing strategy. Most of its products are offered with zero or minimal fees to the customer. For example, no annual fee on credit cards, no monthly fee on accounts, free transfers, etc.. This dramatically lowers the cost barrier for customers, particularly the previously unbanked or underbanked, to join Nubank. Instead of charging customers, Nubank monetizes primarily through interchange and interest spreads, essentially capturing revenue from the payments ecosystem and borrowers rather than via account fees. This model was initially ‘subsidized’ by venture capital and IPO funds while Nubank scaled; the bet was that high customer growth and engagement would eventually yield robust revenue per user through cross-sell and increased share of wallet.

Pricing structure – the counter-positioning advantage

Nubank’s revenue model relies on indirect monetization. Credit card interchange is paid by merchants while customers pay nothing for the card, but Nubank earns fee income whenever they spend. Similarly, interest on credit or late fees are only paid by those who borrow or miss payments, and Nubank’s personal loan interest rates are competitive with or lower than incumbents for comparable credit profiles.

Nubank also introduced opt-in paid services like the NuRewards subscription (for enhanced rewards) and has a tiered interest on deposits. Overall, the pricing strategy is to eliminate traditional fees such as account fees, card annuities, etc. – which incumbents relied on for profit – and replace that revenue by expanding volume such as transactions and loans and taking a slice of those flows. This was a classic disruptive play: incumbents couldn’t easily drop their fees without hurting their own P&L, giving Nubank a counter-positioning advantage.

Even as Nubank grows, it has maintained a customer-friendly pricing stance, for example paying above-market savings rates to depositors in 2022’s high-rate climate while still lowering its funding cost due to efficiency. Therefore, Nubank has pricing power afforded by its low-cost structure. It can offer better deposit rates or lower loan rates than peers and still profit, effectively undercutting competitors.

That leads to high dependence on Interest Income Revenue

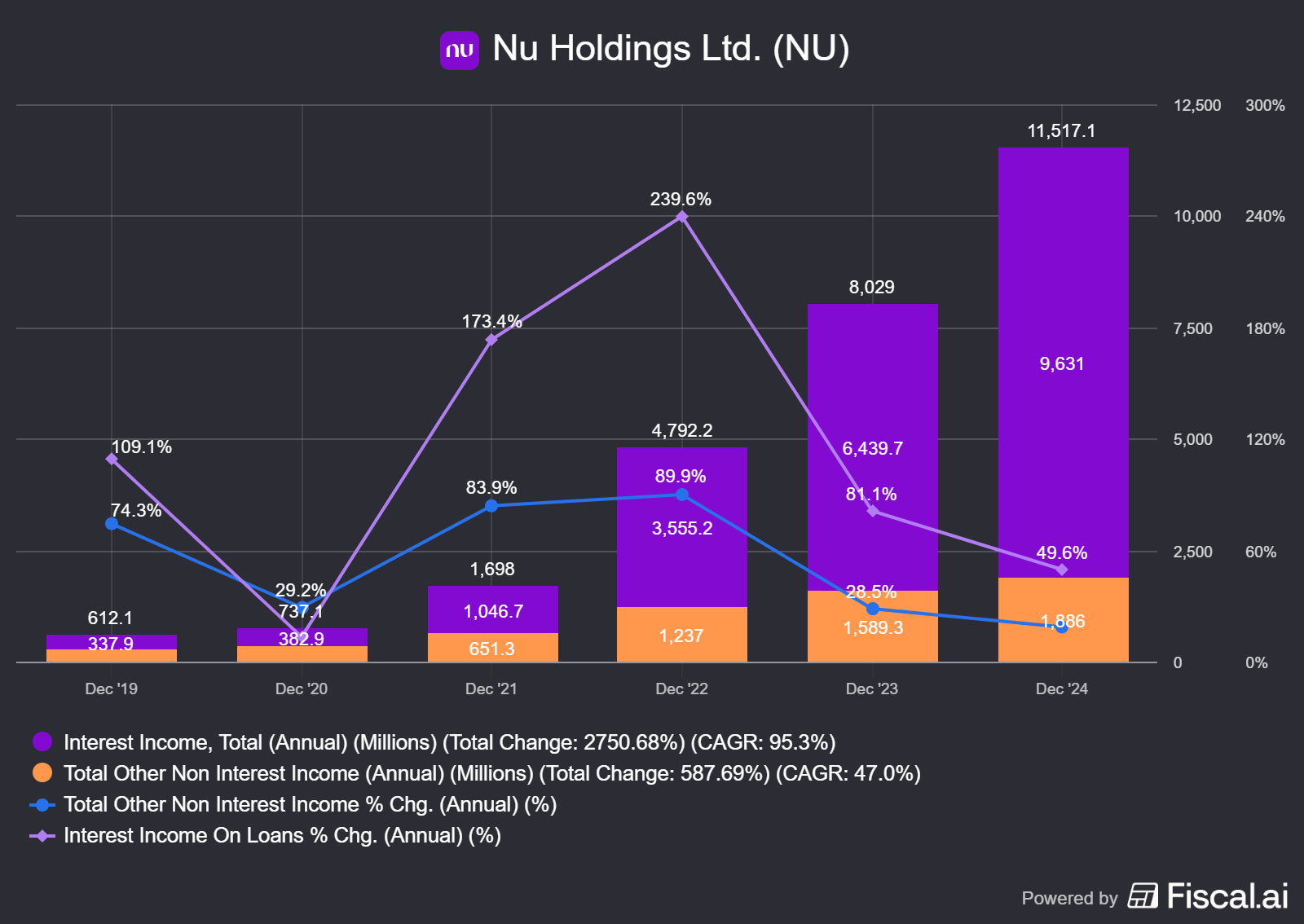

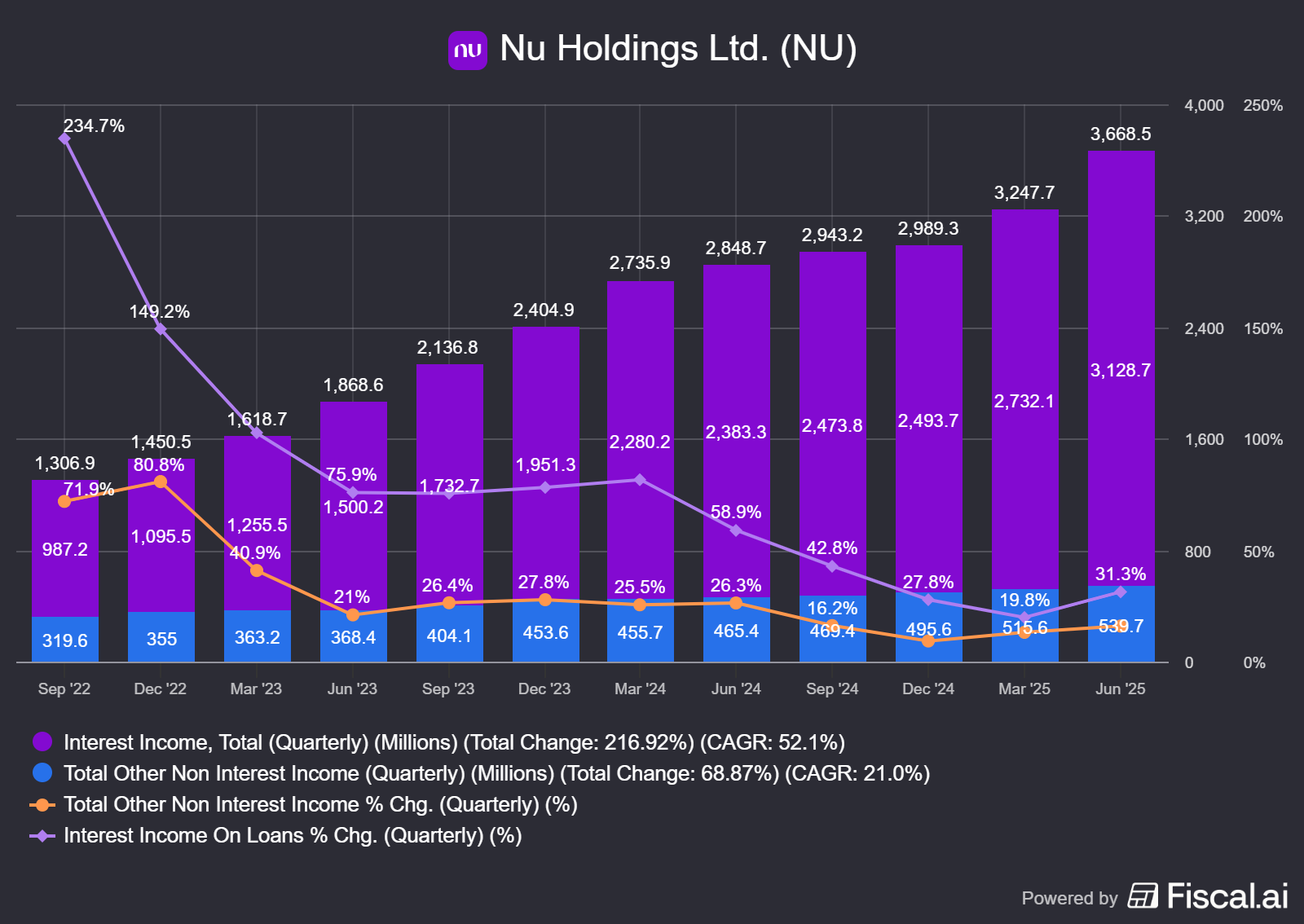

Nubank generates revenue primarily from two main sources: fees and interest income. The revenue mix has shifted toward interest income. In 2020, fees and commissions made up almost 50% of revenue, but by 2024 interest income and fair value gains represented 83% of total revenue. This reflects Nubank’s rapid growth in its lending and credit card portfolios and the high interest rate environment in Brazil during 2022 - 2023.

The expansion of interest share is evident: Nubank’s deposits are increasing heavily with YoY percentages of 48% between Q1 2024 and Q1 2025.

Nubank expects the revenue mix to re-balance longer term as newer fee-generating services such as NuShopping, NuInsurance and NuTravel scale up and as interchange volumes grow with customer spending. The company explicitly notes it anticipates credit card revenue concentration to decline over time with product and regional diversification.

Fee and Commission income

Nubank generates non-interest revenue mainly from interchange fees on card transactions, along with smaller fees from services like its premium subscription, insurance brokerage commissions, and other partnerships. Key drivers for fee income include cross-selling of services such as insurance or mobile phone top-ups through Nubank’s app. These fee drivers appear sustainable given Nubank’s expanding active customer base and engagement.

Net Interest Income – NII & NIM

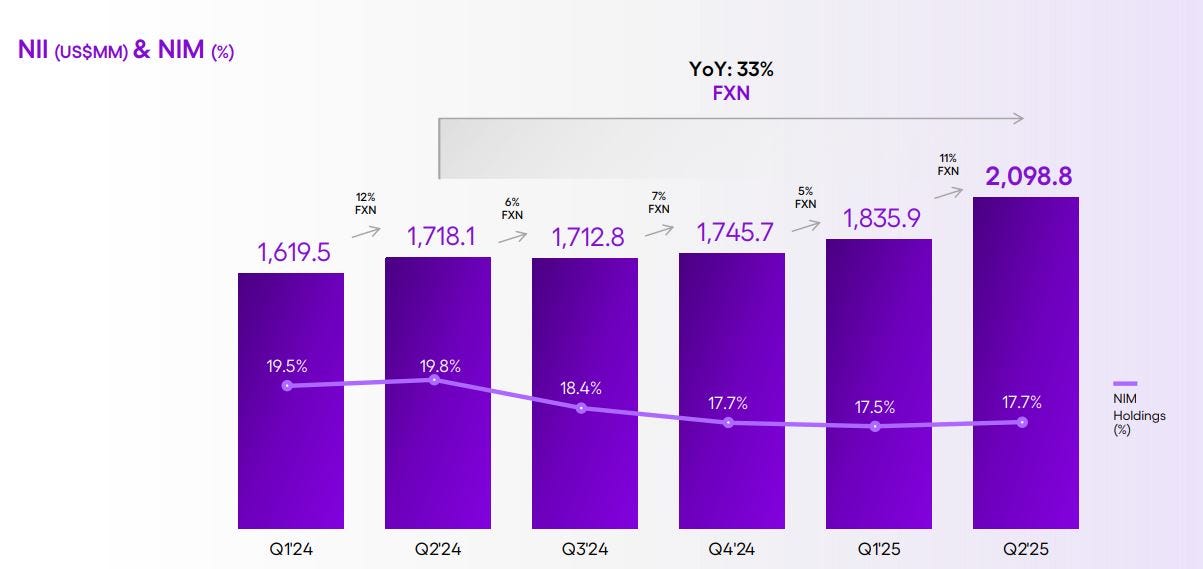

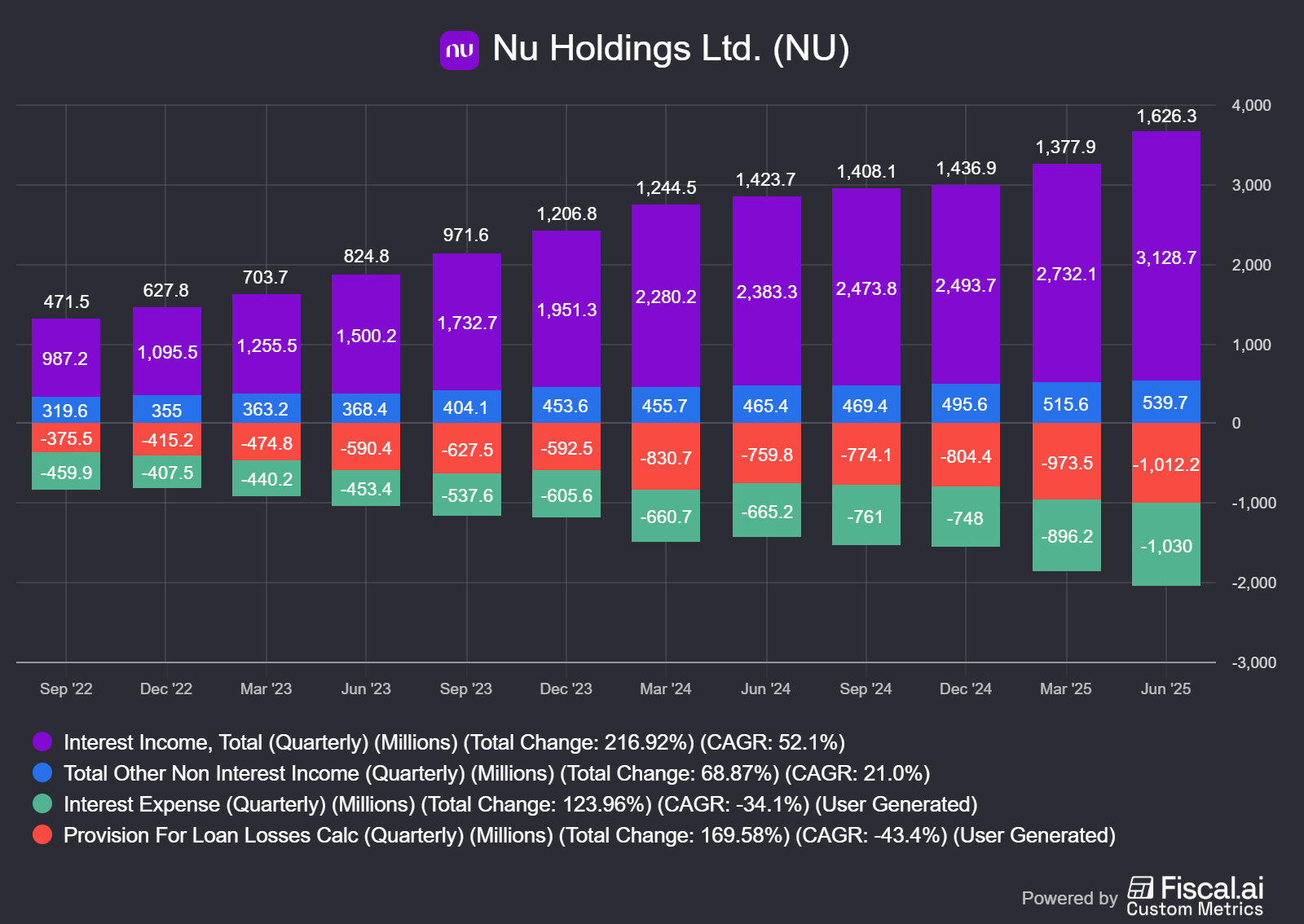

Nubank’s interest income is derived from credit card revolving balances, personal loans, and interest on its investment of excess cash - primarily in government bonds. Interest income soared from 1.05 billion dollar in 2021 to 6.8 billion dollar in 2024.

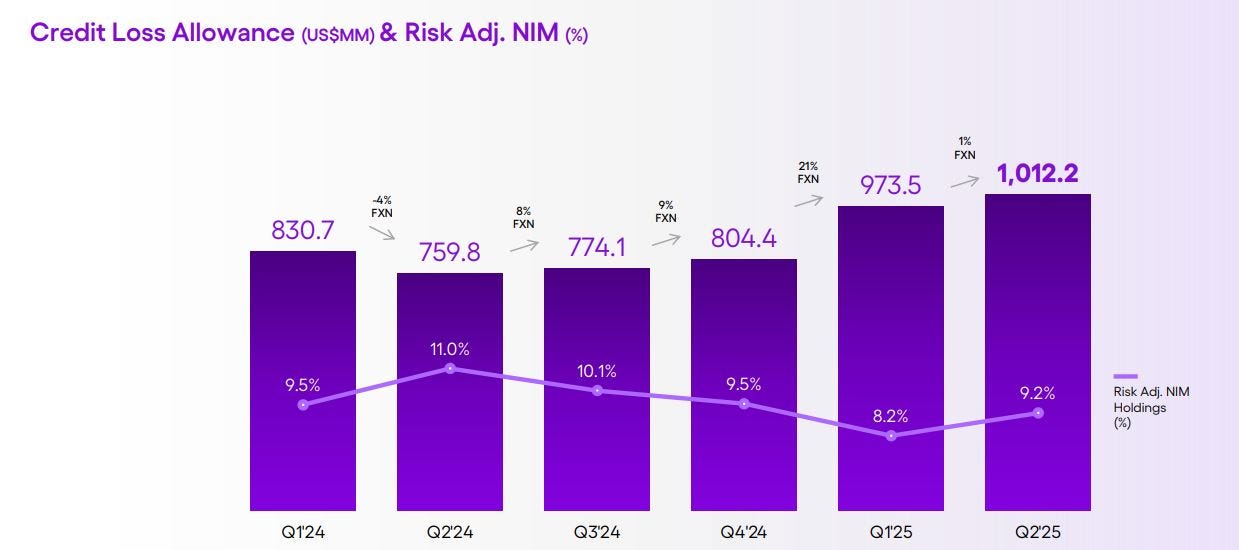

Nubank’s NIM is exceptionally high relative to traditional banks at ca. 17 - 18% versus high-single digits for major Brazilian incumbents, due to its focus on unsecured consumer lending and a low-cost funding base. Even risk-adjusted NIM (net interest minus credit losses) was ca. 9 - 10% in recent quarters, versus 5 - 6% range at incumbents.

Nubank’s outsized NIM comes from its product mix, credit card and consumer loans in Brazil often carry annual interest well above 50%, whereas its deposit costs are around 90% of CDI. Another factor is that Nubank historically held a lot of non-earning cash; as it deploys more cash into loans, reported NIM improves.

Such NIM levels underscore the profitability of its lending, though sustaining them will depend on credit performance and interest rate trends.

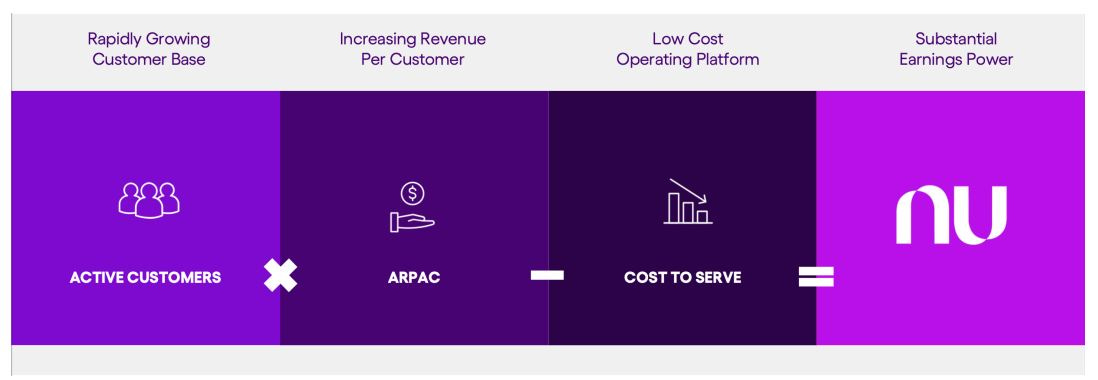

LTV - Lifetime Value

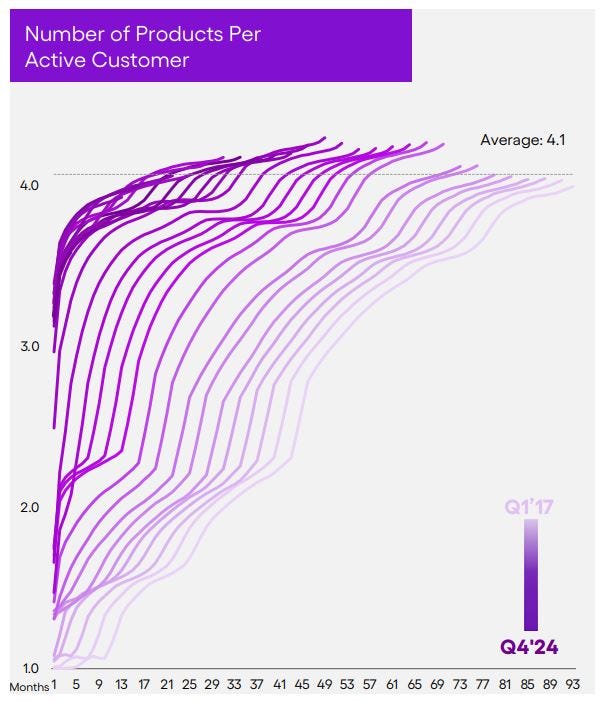

Nubank’s model is built on maximizing the lifetime value (LTV) of each customer through cross-selling and deepening engagement. The company’s data shows that the longer a customer stays, the more products they use and the more revenue they contribute. On average, an active Nubank customer used 4.1 different products in 2024, up from fewer in earlier years. Importantly, 61% of active customers now consider Nubank their primary financial institution, which correlates with higher balances and product uptake.

ARPAC - Average Revenue Per Active Customer

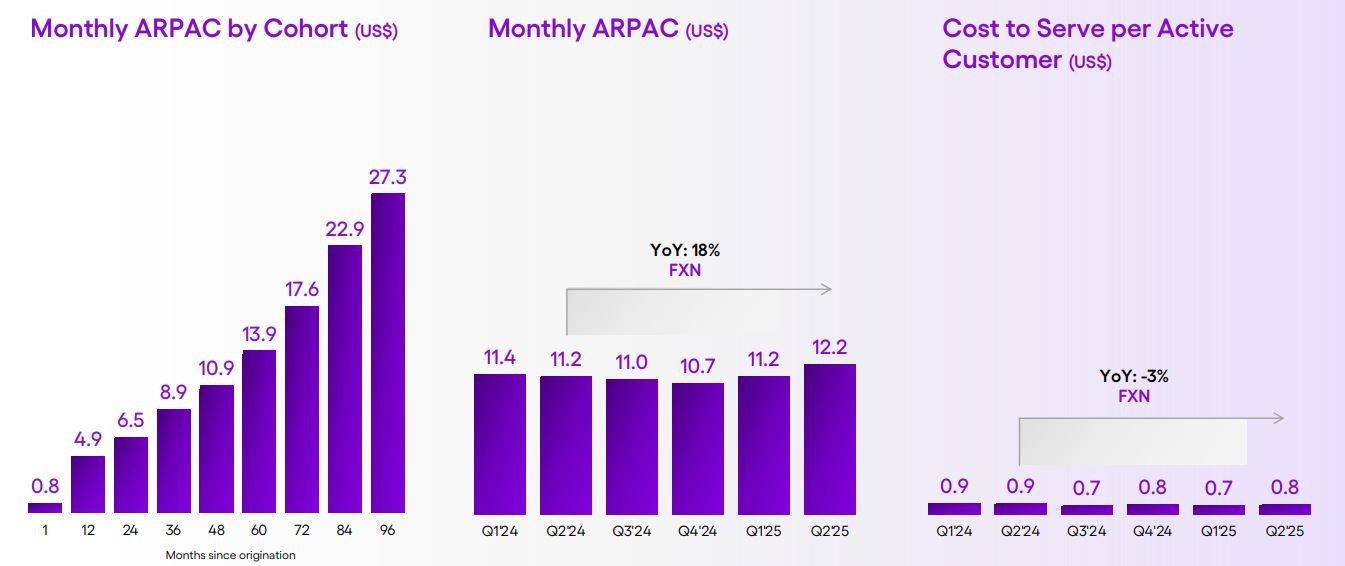

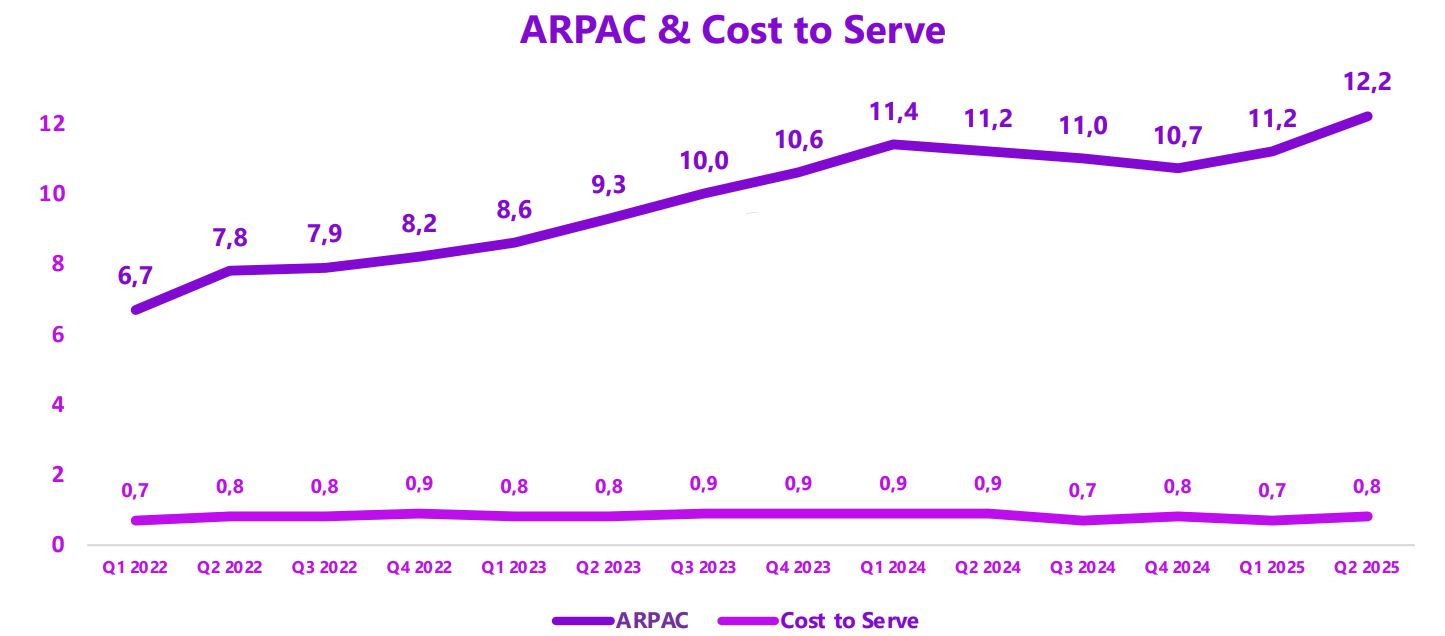

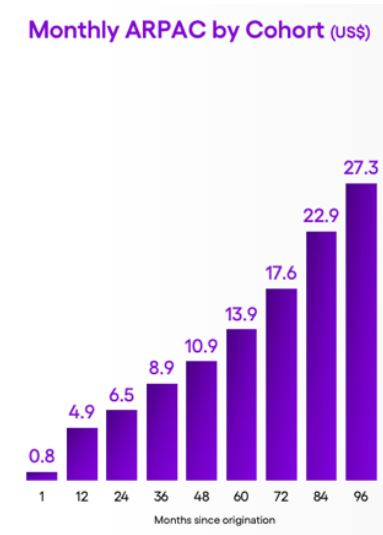

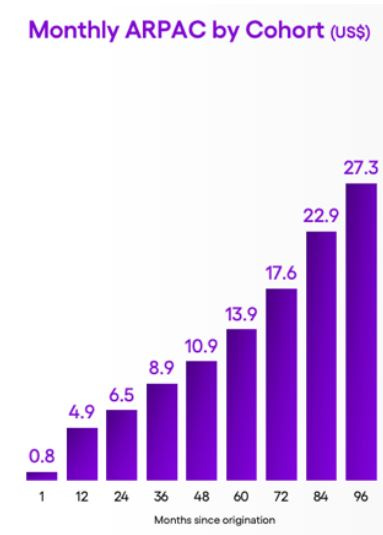

Monthly Average Revenue Per Active Customer (ARPAC) is a key metric used by Nubank to monitor the average monthly revenue generated by each active customer. Nubank’s monthly ARPAC grew from USD 4 in Q2 2021 to USD 12.2 in Q2 2025. As customers use their credit responsibly, Nubank increases their credit limits, which encourages higher spending and in turn drives greater revenue for the company. At the same time, customers become increasingly familiar with Nubank’s products and begin to spend more frequently on the platform. This deeper relationship often leads to the adoption of additional Nubank financial products; as customers engage with multiple products, the company sees a substantial boost in the revenue earned per user. Cohort analysis reveals that this pattern persists over time, with most customer cohorts ultimately surpassing a monthlyARPAC of USD 27 in their 8th year of activity.

Cost to Serve per Active Customer

The average cost to serve each customer remains stable at about USD 0.80 per month during the last years. This dynamic, rising ARPAC while cost per customer stays flat, showcases powerful operating leverage in Nubank’s model.

The company has effectively no marginal customer acquisition cost for referrals and very low marginal servicing cost (the app and cloud infrastructure scales cheaply), so each additional product or account a customer adopts contributes almost entirely to margin. Nubank highlighted that its cost to serve plus G&A per active customer is ca. 85% lower than incumbent banks’. Concretely, a traditional bank might spend more than $4 per customer per month on branches, staff, etc., while Nubank spends less than $1. This cost advantage allows Nubank to offer better pricing and still achieve profitability.

What are the main Unit Economics?

CAC vs LTV

With Customer Acquisition Cost (CAC) between $5 – 10 and annual revenue per active customer around $146 and growing, the payback period on customer acquisition is very short, just half a month(!) of ARPAC covers CAC. With average customer lifespan likely to be many years, and increasing product adoption, the LTV / CAC ratio is enormous, supporting aggressive growth without cash burn.

Margin per Customer

Monthly cost to serve of $0.8 and ARPAC $12.2 in Q2 2025 yields a gross margin per customer of $11.3 per month, or $135 per year, before operating expenses. Given operating expenses per customer continue to decline with scale, more of this gross profit flows to the bottom line each year.

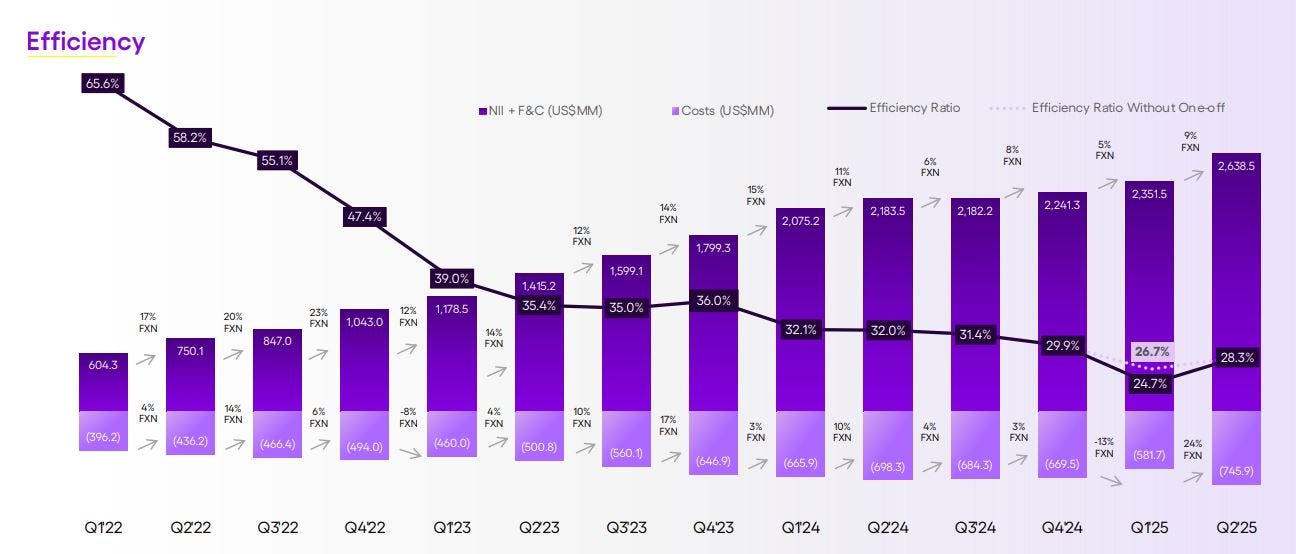

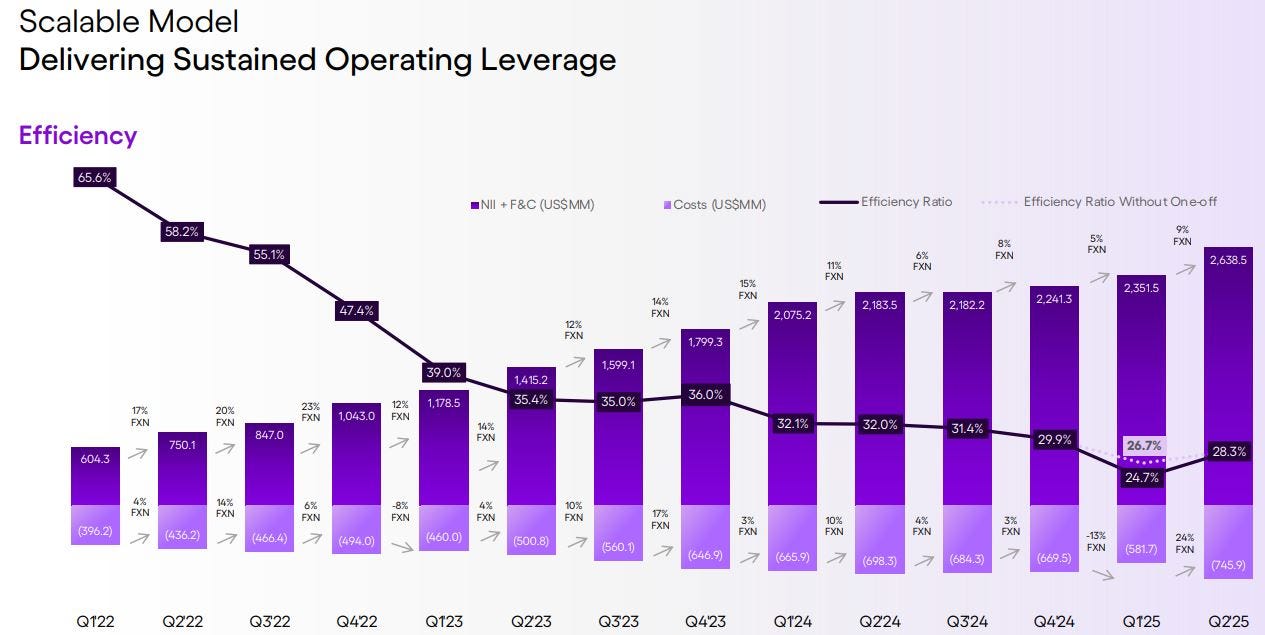

Efficiency Gains

The efficiency ratio (cost / revenue) improved to about 28.3% by Q2 2025 on a banking basis excluding provisions. This trajectory shows that as Nubank scales, incremental revenue comes at high incremental margin. For example, revenue grew 67% in 2023, but operating expenses grew only ca. 30%.

Profitability

Nubank turned the corner on profitability by mid-2022. Currently, Nu bank has an impressive net profit margin of 17.4%. The high ROE of 28% is evidence of the strong per-unit profitability now that the business has reached scale. This profitability emerged much faster than typical fintechs. Nubank is already one of the most profitable banks in the world on an ROE basis, despite its young age.

Strategy and Moat

Nubank frames its entire operating model around four core principles that guide its culture, strategy, and execution. Together, they explain how the company scaled rapidly, disrupted incumbents, and built one of the most efficient and customer-loved banking platforms in the world, and will continue to do in the future.

Mission Driven Culture

Nubank was founded with a clear mission: fight complexity and empower people. This mission is woven into its organizational culture. Every team is expected to ask how their work advances financial inclusion and improves lives. The company actively recruits and retains employees who resonate with its purpose, creating a sense of ownership and alignment across the organization. This principle also drives Nubank’s long-term orientation: prioritizing sustainable customer trust and financial inclusion over short-term profit maximization. The result is a culture where mission comes before bureaucracy, and decisions are filtered through the lens of impact on customers and society.Extraordinary Customer Experience

Nubank strives to deliver financial services that people actually love using, a radical concept in Latin America’s historically unfriendly banking sector. Products are designed to be simple, transparent, and free of hidden fees, directly addressing the frustrations customers had with incumbents. The app provides real-time control, intuitive interfaces, and fast onboarding. Customer service emphasizes empathy, speed, and effectiveness, helping Nubank achieve a Net Promoter Score (NPS) near 90, far higher than traditional banks. This focus on extraordinary experiences has turned customers into promoters, fueling Nubank’s viral, low-cost growth.Advanced Technology

Nubank operates as a technology company with a banking license, not the other way around. It built its core systems in-house, using cloud-native infrastructure that scales seamlessly to tens of millions of users. Proprietary platforms allow rapid product launches, high reliability, and low operating costs. The company invests heavily in engineering and product talent globally, often through acquisitions of specialized firms such as Cognitect, Plataformatec and Hyperplane AI. This technology-first principle ensures Nubank remains more agile, efficient, and innovative than incumbents tied to legacy systems.Proprietary Data Science

Data is embedded in every function of Nubank, turning its massive customer base into a competitive advantage. AI and machine learning models assess thin-file or first-time borrowers, enabling financial inclusion while controlling risk. In addition, Nubank focusses heavily on fraud detection by real-time monitoring systems to flag behavioral patterns anomalies instantly. Data driven insights tailor credit limits, product offers, and app experiences to each user. Finally, by forecasting models Nubank optimizes collections, marketing spend, and resource allocation.

With 120 million customers generating billions of monthly transactions, their proprietary data models compound over time, reinforcing its risk-adjusted profitability and product adoption.

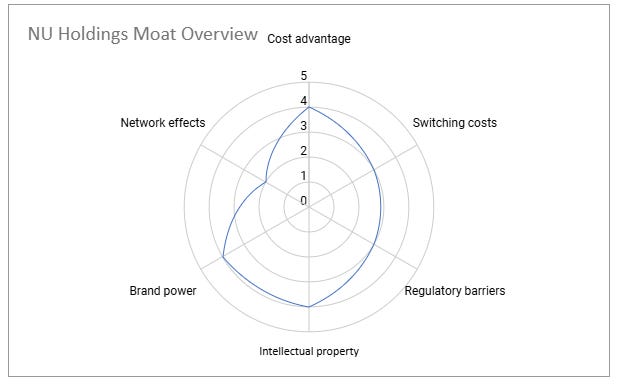

Moats

NU Holdings (Nubank) has built a competitive position in Latin America's digital banking sector through a combination of technological innovation, customer-centric execution, and scale. However, its moats are tested against both traditional incumbents and emerging fintech/neobank rivals.

Switching Costs (Rank: 3)

Switching costs for Nubank are moderate, creating some stickiness through ecosystem integration and habit formation. In retail banking, costs are low on paper, customers face no fees or contracts to leave, and many in Latin America use multiple providers. However, Nubank builds "soft" barriers as users bundle services: salary deposits in NuConta, savings in investments, and bills paid via the app. The longer customers engage, the more entwined Nubank becomes with their finances, with ARPAC rising over time due to increased product usage.

For example, shifting all activities (e.g., credit cards, loans, payments) to a competitor requires effort, new setups, and trust-building. Compared to peers like Banco Inter (with higher complaint rates), Nubank's seamless experience amplifies this moat. Still, it's not insurmountable, dissatisfied users could migrate gradually, and it strengthens primarily against incumbents rather than agile fintechs.Cost Advantage (Rank: 4)

Nubank enjoys significant cost advantages driven by its scale economies and efficient digital model. With over 123 million users across Brazil, Mexico, and Colombia by mid-2025, Nubank is the largest digital bank outside Asia. This massive customer base allows it to spread fixed costs thinly, achieving an average cost per customer of USD 0.8 and an efficiency ratio of 28.3%, far below the 40-50% at traditional banks with branch networks. Nubank's branchless, cloud-based platform contrasts with incumbents' high overheads, enabling lower operational costs.

Among neobank competitors, Nubank's scale remains unmatched in Latin America. For instance, Brazil's Banco Inter has about 33 million customers (one-third of Nubank's), while others like PagBank or C6 Bank lag further. In Mexico, Nubank's 7+ million customers outpace local startups like Albo or Klar, providing cross-selling synergies that smaller rivals lack. Nubank shares these economies with customers via low/no fees, saving users $11 billion in 2023, fostering loyalty. However, this advantage is mainly against incumbents; as fintech peers grow, the gap may narrow, though Nubank's first-mover lead sustains it for now.Regulatory Barriers (Rank: 3)

Regulatory barriers provide Nubank a moderate moat, favoring established players like it over smaller entrants. Navigating Latin America's complex financial regulations (e.g., obtaining banking licenses) impedes newcomers, as seen in Nubank's full licenses in Brazil and Mexico, with Colombia in progress. These are not exclusive but require significant compliance expertise and capital, which Nubank has built through scale and execution.

Regulations generally benefit incumbents and scaled institutions, presenting hurdles for smaller fintechs aiming for market share. For Nubank, this bolsters its position, especially in secured lending like payroll loans. However, competitors like Mercado Pago also hold licenses, so this isn't a unique cornered resource. Against pure startups, it's stronger, but as neobanks mature, the barrier may weaken, though Nubank's track record in multi-country expansion (e.g., rapid Mexican growth) gives it an edge.Brand Power (Rank: 4)

Brand power is one of Nubank's strongest moats, built on its identity as a customer-friendly disruptor. From its purple "Roxinho" card becoming a status symbol in Brazil, Nubank has cultivated emotional loyalty. It ranked as Brazil's Strongest Brand in 2022-2023, outpacing heritage names, and is among the top 10 "most loved" brands. NPS around 90 (three times incumbents') drives 80% word-of-mouth acquisition, lowering costs.

This "cool factor" appeals to younger users, often compared to Amazon or Starbucks in devotion. Surveys show Nubank as "more customer-obsessed than Amazon." Among neobanks, it stands out, Banco Inter lacks the same emotional pull. However, this stems partly from first-mover status; as competitors mature, branding may dilute slightly, but Nubank's consistent delivery (e.g., no-fee products) sustains it.Intellectual Property (Rank: 4)

Nubank's intellectual property moat is strong, rooted in proprietary processes and technology like its NuX credit engine. This AI-driven system analyzes customer behavior and alternative data for dynamic underwriting, enabling Nubank to lend to underbanked segments with lower defaults than peers. Competitors lacking similar data/experience may incur higher losses replicating this reach.

Nubank's cloud-native infrastructure allows rapid updates and scalability, with 100% in-house development fueling agility. Customer service processes, blending AI self-service with "Xpeers" agents, achieve 94% first-call resolution within 45 seconds, hard to emulate. Product innovation, like transaction financing (e.g., Pix Financing), stems from these refined algorithms. While not patented in a traditional sense, this "process power" creates a moving target: systems improve daily with more data. Against fintech peers like Banco Inter (less optimized), it's a differentiator; incumbents struggle to match the tech sophistication. Over time, this could strengthen as Nubank refines further.Network Effects (Rank: 2)

Network effects are limited but present indirectly through data and community. Direct effects (e.g., user-to-user value) are minimal in banking, but Nubank's referral flywheel—happy users recruiting via word-of-mouth—creates organic growth, with NPS fueling low acquisition costs.

A stronger indirect effect comes from data: more users generate richer insights for better underwriting and products, attracting more customers in a virtuous loop. For instance, refined risk models from 123 million users enable inclusive lending. However, this isn't classic network economies like platforms (e.g., Mercado Pago's e-commerce ties). Peers like PagSeguro have stronger merchant networks. Overall, it's modest and may not widen significantly against scaled competitors.

Nubank's overall moat is solid (average ~3.3/5) against incumbents but less assured long-term against fintechs. Strengths in cost, IP, and brand provide durability, but scaling rivals could challenge sustainability in 10 years. Focus on process innovation and ecosystem depth will be key.

Competition – mix between Incumbents and Fintech

Direct competitors to Nubank include incumbent banks and neobanks offering similar retail banking products (credit cards, payment accounts, consumer loans). These players directly approach the same customers and deposits, from Itaú and Bradesco in Brazil to BBVA in Mexico and Bancolombia in Colombia, as well as digital-only peers like Inter, Stori, or Nequi that mirror Nubank’s app-based model.

Indirect competitors include fintech and non-bank entities that fulfill specific financial needs, potentially siphoning off parts of Nubank’s business. These can be categorized in:

Payment-focused apps and wallets: Pix in Brazil, Oxxo’s Spin in Mexico, RappiPay in Colombia

Merchant credit providers e.g. Mercado Pago or store cards

Specialty lenders/fintechs that offer substitutes for bank credit (such as BNPL providers and micro-lenders). These don’t offer a full banking suite but compete in niches like payments or point-of-sale financing.

Substitute providers can also be considered, notably the informal or cash economy that still serves many underbanked consumers in Latin America. For instance, reliance on cash services like convenience-store payment vouchers in Mexico or informal lenders is effectively a substitute for formal banking for some consumers – and part of Nubank’s mission is to convert these users into banking clients.

Brazil

Nubank’s home market of Brazil features both powerful incumbent banks and agile fintech challengers. The “Big Five” traditional banks long dominated retail banking with vast branch networks and full-service offerings. These incumbents are direct competitors in products like credit cards and consumer loans, although they historically focused on more affluent and corporate segments:

Itaú Unibanco

Bradesco

Banco do Brasil

Caixa Econômica

Santander Brasil

Alongside them, a wave of neobanks and fintechs has emerged as direct competitors to Nubank’s digital model. All of them offer app-based accounts and credit cards with low fees similar to Nubank.

Key digital-first rivals include: Banco Inter, a former mid-tier bank turned into a fully digital lender, C6 Bank, Neon and Will Bank.

Payment focused fintechs are indirect competitors, such as Mercado Pago, PicPay and PagSeguro/PagBank.

They offer substitute services like e-wallets, payment processing, and merchant credit. Nubank also faces competition from store-based lenders (e.g. Banco PAN targeting low-income borrowers) and the rapid adoption of Pix (the Central Bank’s instant payment system), which, while not a single competitor, has become an alternative to card transactions for millions of Brazilians.

Nubank has rapidly grown its share in Brazil’s key product segments, although incumbent banks still command a majority of financial assets. In the credit card market, Nubank’s ascent has been striking – it is now the #2 issuer by volume of credit card loans, holding about 12.9% of market share as of March 2024. Itaú Unibanco remains the leader with ~24.3% share of card purchase volume, while Bradesco is close to Nubank at 12.5%. By number of cards issued, Nubank has become one of the top issuers in Brazil.

In deposit accounts and customer base, Nubank’s scale is similarly impressive: by serving 107 million people in Brazil, it is almost double as big as Brazil’s largest traditional bank, Itaú, who serves an estimated 55 - 60 million customers globally. However, when measured by financial volumes (like total deposits or loans), Nubank’s share is more modest: it holds 36.6 billion in deposits (as of Q2 2025), which is a single-digit percentage of Brazil’s banking system deposits since the top five banks collectively hold hundreds of billions in assets.

In personal lending, Nubank’s loan book - 27.3 billion dollar in credit portfolio in Q2 2025 - remains smaller than incumbents’, though it is expanding fast (40% YoY). Segments where competitors dominate include mortgages and auto loans. Nubank does not (yet) offer home or car loans, leaving traditional banks like Caixa and Banco do Brasil to dominate those categories. Likewise, high-net-worth wealth management and large corporate banking are outside Nubank’s focus and remain the focus of incumbents. Nonetheless, within unsecured consumer credit and daily banking transactions, Nubank has captured significant share.